Table of contents

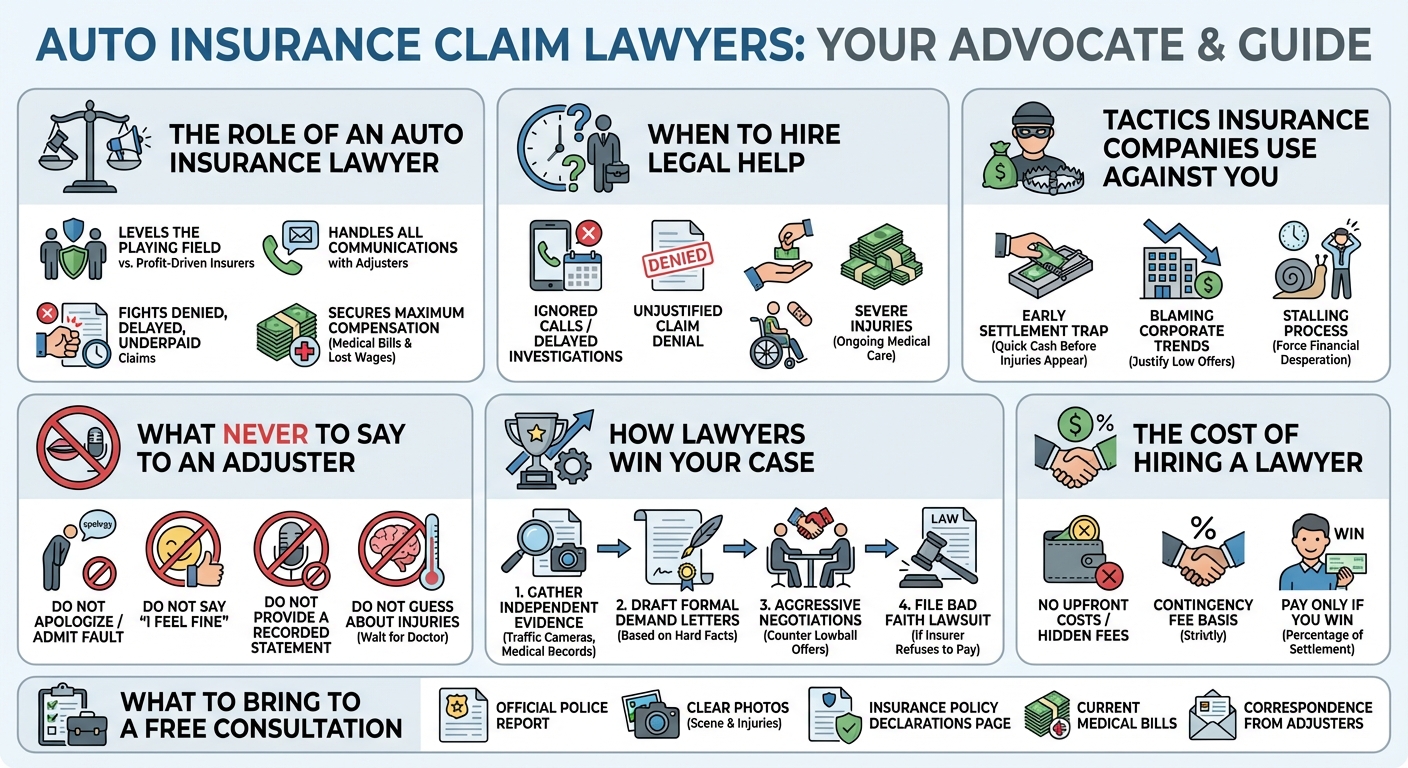

An auto insurance claim lawyer represents policyholders and accident victims when insurance companies deny, delay, or underpay valid claims. These attorneys handle all adjuster communications, gather critical evidence, and negotiate aggressive settlements to ensure you receive full compensation for medical bills, property damage, and lost wages.

Why You Need an Auto Insurance Claim Lawyer

After a car crash, you expect your insurance policy to provide the financial safety net you paid for. Unfortunately, insurers prioritize their profit margins over your recovery. Hiring an auto insurance claim lawyer levels the playing field, ensuring you have a dedicated advocate to fight back against unfair denials, delays, and lowball offers.

The difference between a standard car accident claim and an insurance dispute

A standard car accident claim involves filing your damages, submitting evidence, and receiving a fair payout. An insurance dispute arises when the insurer actively resists fulfilling its obligations. This can involve disputing who is at fault, questioning the necessity of your medical treatments, or arguing that your policy does not cover the specific damages claimed. When a routine claim turns adversarial, legal intervention becomes necessary.

Signs your insurance company is acting in bad faith

Insurance companies are legally bound to process claims in good faith. If your insurer is ignoring your calls, failing to investigate the crash promptly, misrepresenting policy language, or offering a settlement drastically lower than your actual damages, they may be engaging in bad faith practices. An attorney can identify these violations and hold the company accountable.

When to escalate from a standard claim to legal action

You should escalate to legal action the moment an adjuster issues an unjustified denial, demands unreasonable documentation, or refuses to negotiate a settlement that covers your medical bills and lost wages. Waiting too long to hire a lawyer can allow the insurer to build a case against you or run down the clock on your statute of limitations.

Is it worth getting an attorney for a vehicle accident?

Yes, getting an attorney for a vehicle accident is highly worth it if you suffered injuries or face a disputed claim. Statistics consistently show that accident victims with legal representation secure significantly higher settlements than those without, as lawyers prevent insurers from using deceptive tactics to minimize your payout.

Comparing settlement offers with and without legal representation

Insurance adjusters use software programs designed to generate the lowest possible payout. When you are unrepresented, they offer a fraction of what your case is worth, assuming you do not know your legal rights. Once an auto insurance claim lawyer steps in, adjusters know they can no longer rely on intimidation. Attorneys calculate the true lifetime cost of your injuries, forcing the insurer to offer a settlement that reflects reality.

Handling severe injuries vs. minor property damage

If your accident resulted only in minor cosmetic damage to your vehicle, you can often handle the claim yourself. However, if you sustained severe injuries—such as closed head injuries, spinal damage, or broken bones—an attorney is essential. Severe injuries require complex medical evidence, long-term care calculations, and aggressive negotiation to ensure you are not left paying out of pocket for future treatments.

Common Tactics Insurance Adjusters Use to Devalue Claims

Insurance adjusters are trained negotiators whose primary goal is to save the company money. They employ a variety of psychological and procedural tactics to devalue your claim before you even realize what is happening.

The ‘Property Damage Trap’ and early settlement offers

Insurers often rush to offer a quick check to cover your vehicle’s property damage, hoping you will sign a release before your physical injuries fully manifest. This early settlement trap is designed to close your bodily injury claim prematurely, leaving you without recourse when you discover you need physical therapy or surgery weeks later.

Using ‘Social Inflation’ as an excuse for lowballing

Insurance companies frequently blame “social inflation”—the idea that jury verdicts and litigation costs are rising—as a blanket excuse to offer lower settlements across the board. An experienced attorney sees through this corporate jargon and focuses strictly on the specific facts, damages, and policy limits of your individual case.

Delaying the investigation process

Delay is a weapon. By dragging out the investigation, losing paperwork, or endlessly transferring your file to different adjusters, the insurance company hopes you will become financially desperate. They know that as your medical bills pile up, you become more likely to accept a lowball offer just to get some immediate relief.

What not to say to an insurance claim adjuster?

Never apologize, admit fault, or say you feel “fine” to an insurance claim adjuster. Avoid providing a recorded statement or speculating about your injuries before receiving a full medical evaluation. Adjusters use these casual statements out of context to devalue your claim or deny coverage entirely.

The dangers of the recorded statement

Adjusters will push you to give a recorded statement under the guise of “moving your claim forward.” In reality, they are fishing for inconsistencies. They will ask leading questions designed to make you downplay your injuries or accidentally accept partial blame. You are not legally required to give the other driver’s insurance company a recorded statement.

Admitting fault or apologizing

Even a polite “I’m sorry this happened” can be twisted into an admission of guilt. Texas and other states use comparative negligence laws, meaning any percentage of fault assigned to you directly reduces your compensation. Let your lawyer handle all communications to protect your liability status.

Speculating about your injuries before seeing a doctor

Adrenaline masks pain. If you tell an adjuster your neck “just feels a little stiff” on the day of the crash, they will use that statement against you when an MRI later reveals a herniated disc. Never discuss your medical condition with an insurer until a doctor has fully diagnosed you.

How an Insurance Dispute Attorney Maximizes Your Settlement

Your lawyer’s job is to build an airtight case that leaves the insurance company with no choice but to pay what they owe.

Gathering independent evidence and medical records

An attorney will not rely on the insurance company’s biased investigation. They will subpoena traffic camera footage, interview eyewitnesses, hire accident reconstruction experts, and compile comprehensive medical records to prove the exact cause of the crash and the full extent of your damages.

Negotiating aggressively with insurance adjusters

Armed with undeniable evidence, your lawyer will draft a formal demand letter. They handle the back-and-forth negotiations, countering the adjuster’s lowball offers with hard facts and legal precedents. This professional buffer protects you from the stress of haggling with corporate representatives.

Preparing for litigation if a fair settlement isn’t reached

The most effective way to secure a high settlement is to show the insurer you are ready for trial. If the insurance company refuses to negotiate fairly, your attorney will file a formal lawsuit, initiating the discovery process and preparing to present your case to a judge or jury.

Is suing your insurance company worth it?

Suing your insurance company is worth it if they operate in bad faith by wrongfully denying, delaying, or severely underpaying your valid claim. A successful lawsuit can force the insurer to pay your original claim, cover your attorney fees, and potentially owe you additional punitive damages.

Understanding breach of contract and bad faith lawsuits

When you sue an insurer, you are typically filing for breach of contract (failing to pay what the policy dictates) or bad faith (unreasonable and deceptive practices). Bad faith claims are particularly powerful because they expose the insurance company’s internal mishandling of your file.

Potential compensation: punitive damages and attorney fees

In a successful bad faith lawsuit, you can recover more than just your original accident damages. Courts may award punitive damages designed to punish the insurance company for egregious behavior, as well as order the insurer to pay your legal fees, maximizing your net recovery.

The timeline of an insurance lawsuit

Litigation takes time. While a standard settlement might take a few months, a lawsuit can take a year or more depending on court schedules and the complexity of discovery. However, simply filing the lawsuit often pressures the insurance company into offering a fair settlement before the trial date arrives.

How much does an insurance claim attorney cost?

An insurance claim attorney typically costs nothing upfront because they work on a contingency fee basis. This means the lawyer only gets paid a percentage of your final settlement or court award. If they do not win or settle your case, you do not owe any legal fees.

Understanding contingency fee agreements

Contingency fees align your lawyer’s interests with your own: the more they recover for you, the more they earn. The standard percentage ranges from 33% to 40%, depending on whether the case settles early or goes to trial. This structure allows anyone, regardless of financial status, to hire top-tier legal representation.

No upfront costs or hidden fees

Reputable auto insurance claim lawyers advance all the costs of building your case, including expert witness fees, court filing costs, and investigation expenses. You will never be asked to write a check out of your own pocket to keep your case moving forward.

Get Help From an Experienced Auto Insurance Claim Lawyer

Do not let a massive insurance corporation dictate your physical and financial recovery. If you are facing a denied claim, endless delays, or an insulting settlement offer, it is time to bring in professional legal firepower.

What to bring to your free consultation

To get the most out of your initial case review, bring a copy of the police report, photographs of the accident scene and your injuries, your auto insurance policy declarations page, all medical bills, and any correspondence you have received from the insurance adjusters.

How to contact our legal team today

Our legal team is ready to review your case, explain your rights, and take over the fight with the insurance company. Contact us today to schedule your free, no-obligation consultation and take the first step toward securing the compensation you deserve.