Table of contents

In most states, the statute of limitations for a car accident lawsuit is two to three years from the date of the crash. However, this legal deadline varies by state, ranging from one to six years depending on local laws and the type of claim.

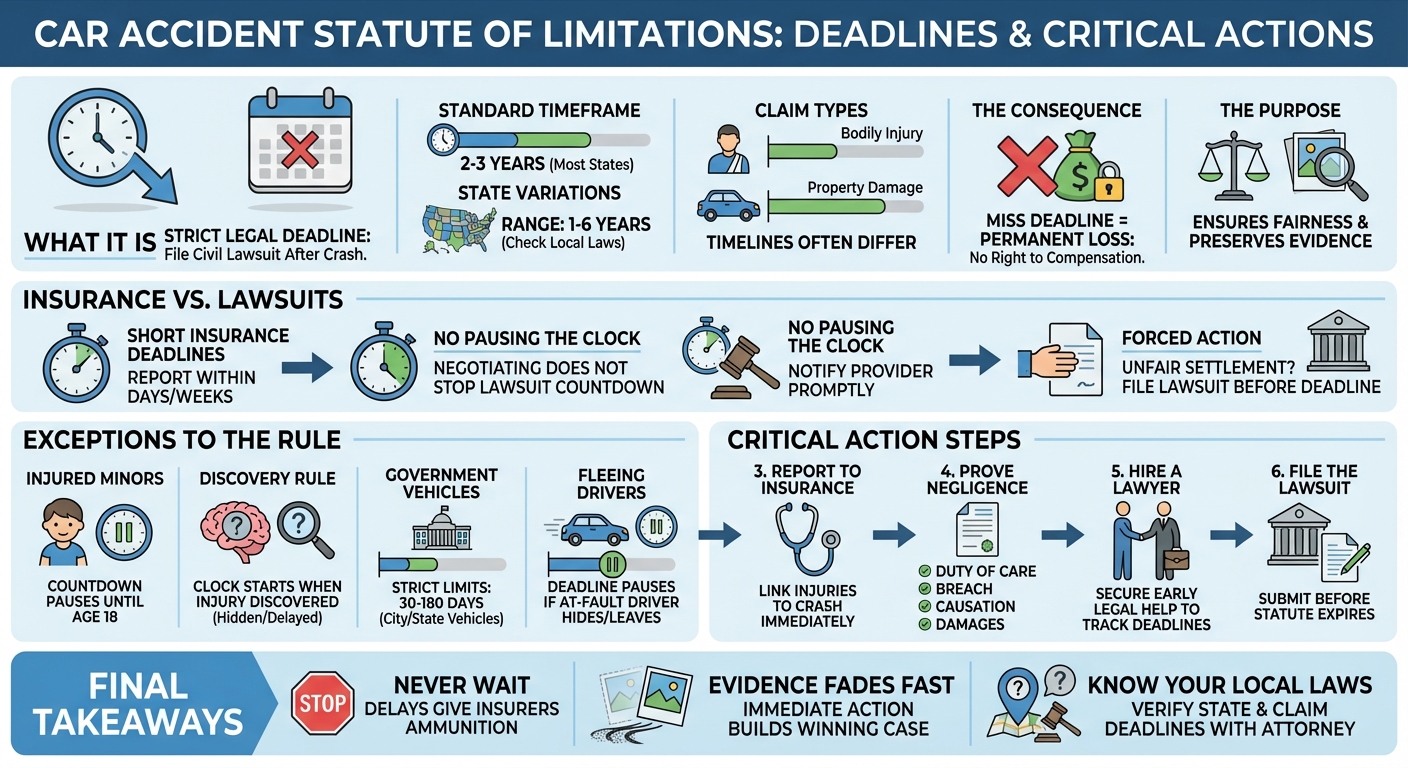

What Is the Statute of Limitations for a Car Accident?

A statute of limitations is a strict legal deadline that dictates how long you have to file a civil lawsuit after suffering harm or property damage. In personal injury law, this clock typically starts ticking on the exact date your car accident occurs.

In most U.S. states, the statute of limitations for a car accident lawsuit is between two and three years. If you fail to file your lawsuit in the appropriate court before this window closes, the judge will almost certainly dismiss your case, and you will permanently lose your right to seek financial compensation from the at-fault driver.

These legal deadlines exist for two primary reasons:

- Evidence Preservation: Physical evidence degrades, and witness memories fade over time. A deadline ensures cases are tried while the evidence is still reliable.

- Legal Fairness: It prevents individuals from having the threat of a lawsuit hanging over their heads indefinitely.

Car Accident Statute of Limitations by State (50-State Guide)

Because personal injury laws are governed at the state level, your filing window depends entirely on where the accident occurred. Furthermore, many states have different deadlines for Personal Injury (PI) claims (bodily harm) versus Property Damage (PD) claims (vehicle repairs).

Below is a comprehensive guide to the standard statutes of limitations across all 50 states. Note: Laws are subject to legislative changes (such as Florida’s recent shift to a 2-year deadline), so always verify with a local attorney.

| State | Personal Injury Deadline | Property Damage Deadline |

|---|---|---|

| Alabama | 2 years | 2 years |

| Alaska | 2 years | 2 years |

| Arizona | 2 years | 2 years |

| Arkansas | 3 years | 3 years |

| California | 2 years | 3 years |

| Colorado | 3 years (Auto accidents) | 3 years |

| Connecticut | 2 years | 2 years |

| Delaware | 2 years | 2 years |

| Florida | 2 years | 4 years |

| Georgia | 2 years | 4 years |

| Hawaii | 2 years | 2 years |

| Idaho | 2 years | 3 years |

| Illinois | 2 years | 5 years |

| Indiana | 2 years | 2 years |

| Iowa | 2 years | 5 years |

| Kansas | 2 years | 2 years |

| Kentucky | 1 year (2 years for auto) | 2 years |

| Louisiana | 1 year | 1 year |

| Maine | 6 years | 6 years |

| Maryland | 3 years | 3 years |

| Massachusetts | 3 years | 3 years |

| Michigan | 3 years | 3 years |

| Minnesota | 2 to 6 years | 6 years |

| Mississippi | 3 years | 3 years |

| Missouri | 5 years | 5 years |

| Montana | 3 years | 2 years |

| Nebraska | 4 years | 4 years |

| Nevada | 2 years | 3 years |

| New Hampshire | 3 years | 3 years |

| New Jersey | 2 years | 6 years |

| New Mexico | 3 years | 4 years |

| New York | 3 years | 3 years |

| North Carolina | 3 years | 3 years |

| North Dakota | 6 years | 6 years |

| Ohio | 2 years | 2 years |

| Oklahoma | 2 years | 2 years |

| Oregon | 2 years | 6 years |

| Pennsylvania | 2 years | 2 years |

| Rhode Island | 3 years | 10 years |

| South Carolina | 3 years | 3 years |

| South Dakota | 3 years | 6 years |

| Tennessee | 1 year | 3 years |

| Texas | 2 years | 2 years |

| Utah | 4 years | 3 years |

| Vermont | 3 years | 3 years |

| Virginia | 2 years | 5 years |

| Washington | 3 years | 3 years |

| West Virginia | 2 years | 2 years |

| Wisconsin | 3 years | 3 years |

| Wyoming | 4 years | 4 years |

Insurance Claims vs. Personal Injury Lawsuits: Knowing the Difference

A common and costly mistake accident victims make is confusing the insurance company’s reporting deadline with the state’s legal statute of limitations.

Insurance Reporting Deadlines Are Shorter: Most auto insurance policies require you to report an accident “promptly” or within a “reasonable time.” In practice, this usually means within a few days to a few weeks. Failing to notify the insurer quickly can result in a denied claim.

Filing a Claim Does Not Pause the Clock: Negotiating with an insurance adjuster does not “toll” (pause) your statute of limitations. If you spend two years arguing over a settlement and the deadline passes, the insurance company will simply walk away, knowing you can no longer sue them.

When Settlement Fails: If the insurance company refuses to offer a fair payout, you must transition from an insurance claim to a formal lawsuit before the statute of limitations expires. Filing the lawsuit is what officially protects your legal rights.

Exceptions to the Rule: Can the Deadline Be Extended?

While the statute of limitations is generally rigid, there are specific legal exceptions that can “toll” or delay the countdown.

- Minors Involved in Crashes: If a child is injured in a car accident, the statute of limitations usually does not begin until they reach the age of majority (typically 18). From their 18th birthday, they will have the standard state timeframe to file a lawsuit.

- The Discovery Rule: Sometimes, injuries are not immediately apparent. For delayed-onset conditions—such as closed head injuries or TMJ injuries resulting from severe whiplash—the clock may start on the date the injury was discovered (or reasonably should have been discovered), rather than the date of the crash.

- Government Vehicles: If your accident involved a city bus, a mail truck, or a state-owned vehicle, your timeline is drastically reduced. You typically must file a formal “Notice of Claim” with the government agency within 30 to 180 days of the accident.

- The Defendant Leaves the State: If the at-fault driver flees the state or goes into hiding before you can serve them with a lawsuit, the court may pause the statute of limitations until they return or can be located.

Why You Shouldn’t Wait Until the Deadline to Take Action

Just because you have two or three years to file a lawsuit does not mean you should wait. Delaying action can severely damage the value of your claim.

First, physical evidence disappears rapidly. Skid marks wash away, traffic camera footage is overwritten (often within 72 hours), and witnesses forget crucial details. Documenting your accident scene immediately is vital to building a winning case.

Second, waiting to seek treatment gives insurance companies ammunition. This is why you should never skip the emergency room after a crash. If you delay medical evaluation, adjusters will argue that your injuries were caused by a separate event or aren’t as serious as you claim.

Finally, early legal intervention protects you from predatory insurance tactics. An attorney can handle independent medical examinations, investigate pre-existing conditions, and ensure your case is perfectly positioned long before the statute of limitations becomes an issue.

Frequently Asked Questions About Car Accident Claims

How long after an accident can you make a claim?

You should report the accident to your insurance company within a few days. However, you generally have two to three years to file a formal personal injury lawsuit, depending on your state’s specific statute of limitations. Missing this legal deadline permanently bars your right to compensation.

Can I sue for an accident that happened years ago?

You can only sue for a past accident if the statute of limitations has not yet expired. While most states allow two to three years, certain exceptions—like the discovery rule for delayed injuries or tolling for minors—might extend the deadline. Otherwise, your claim is legally barred.

What are the 4 things required to prove negligence?

To successfully prove negligence in a car accident claim, you must establish four critical elements: duty of care, breach of that duty, causation, and damages. You must show the at-fault driver owed you safe driving, failed to provide it, directly caused your crash, and inflicted quantifiable losses.

What to do with a $500,000 settlement?

After receiving a large settlement, first ensure all medical liens, legal fees, and taxes are fully paid. Next, establish an emergency fund and pay off high-interest debt. Finally, consult a financial advisor to invest the remaining funds strategically, ensuring long-term financial stability and covering future medical needs.

Protecting Your Right to Compensation After a Crash

The statute of limitations is the most critical deadline in your car accident case. Whether you have one year or six, allowing this window to close means losing your only leverage against the at-fault driver and their insurance company.

Hiring an experienced car accident lawyer early in the process ensures you never miss a critical deadline. They will track the statute of limitations, handle all insurance communications, and file your lawsuit promptly if a fair settlement cannot be reached. If you have been injured, your next step should be evaluating your specific case timeline with a qualified legal professional.