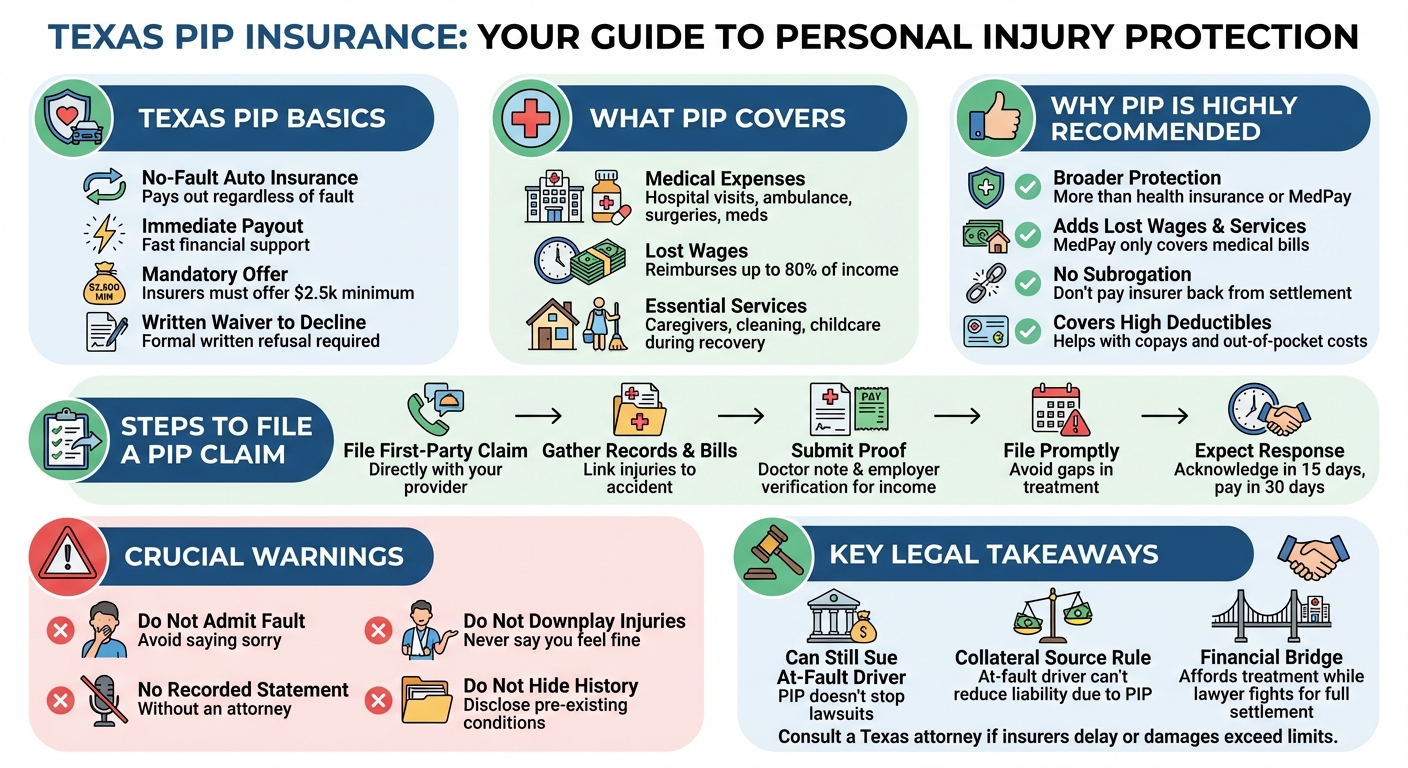

In Texas, Personal Injury Protection (PIP) is a no-fault auto insurance coverage that pays for medical expenses, 80% of lost wages, and essential services after a car accident. Texas law requires insurers to offer at least $2,500 in PIP coverage, which can only be declined in writing.

Navigating PIP Insurance in Texas: The Complete Guide

After a car accident in Texas, the immediate aftermath is often chaotic. Between securing a police report, seeking emergency medical care, and dealing with vehicle damage, the financial stress can mount quickly. Personal Injury Protection (PIP) insurance is designed to be your first line of financial defense, providing immediate relief while the broader liability claims are sorted out.

What is Personal Injury Protection (PIP) in Texas?

Personal Injury Protection, commonly known as PIP, is a specific type of auto insurance coverage available to Texas drivers. It is designed to cover out-of-pocket expenses resulting from a car accident, providing a financial safety net for you and the passengers in your vehicle.

The Texas Law: Minimums and Written Waivers

Under the Texas Insurance Code, all auto insurance companies are legally required to offer PIP coverage to policyholders. The minimum coverage amount required to be offered is $2,500 per person, though drivers can opt for higher limits such as $5,000 or $10,000. While the offering is mandatory, purchasing it is not. However, to decline PIP coverage, a Texas driver must sign a formal written waiver. If your insurance company cannot produce this signed waiver after an accident, Texas law presumes you have PIP coverage.

Why PIP is Considered No-Fault Insurance

PIP is strictly a no-fault insurance policy. This means it pays out regardless of who caused the collision. Whether you were rear-ended at a red light or accidentally caused a fender bender yourself, your PIP benefits remain accessible. This no-fault nature allows for rapid payouts, bypassing the lengthy investigations required to establish liability in a standard personal injury claim.

How does PIP coverage work in Texas?

In Texas, PIP coverage works as a no-fault insurance policy that pays for your medical bills, 80% of lost wages, and essential services after a car accident, regardless of who caused the crash. You file a claim directly with your own auto insurer to receive these benefits.

Filing a First-Party Claim with Your Own Insurer

Because PIP is first-party coverage, you do not deal with the at-fault driver’s insurance company to access these funds. Instead, you file the claim directly with your own insurance provider. You will need to submit documentation of your expenses, which your insurer processes independently of any third-party liability claims you might be pursuing.

Timeline for PIP Payouts in Texas

Texas law imposes strict deadlines on insurance companies handling PIP claims. Once you submit your proof of loss (such as medical bills or wage verification), the insurance company generally has 15 days to acknowledge the claim and 30 days to pay it. If they fail to meet these deadlines, they may be subject to penalties, including interest on the delayed payments.

What Exactly Does Texas PIP Insurance Cover?

PIP is highly versatile and covers a broader range of expenses than standard health insurance or Medical Payments (MedPay) coverage.

Reasonable Medical Expenses

PIP covers all reasonable and necessary medical expenses arising from the accident. This includes ambulance fees, emergency room visits, surgeries, hospital stays, physical therapy, chiropractic care, and prescription medications. It covers you, your covered family members, and any passengers in your vehicle at the time of the crash.

Lost Wages (The 80% Rule)

If your injuries prevent you from working, PIP provides critical income replacement. In Texas, PIP will reimburse up to 80% of your lost wages. This applies whether you are a salaried employee, an hourly worker, or an independent contractor, provided you can supply sufficient documentation of your lost income.

Essential Services and Caregiver Costs

One of the most overlooked benefits of PIP is its coverage for essential services. If your injuries leave you unable to perform normal household duties, PIP can pay for a caregiver, a house cleaner, lawn maintenance, or childcare services during your recovery period.

Is PIP worth it in Texas?

Yes, PIP is highly worth it in Texas. It provides immediate, no-fault financial relief for medical bills and lost wages while you wait for a third-party settlement. Because it covers 80% of lost income and essential services, it offers broader protection than standard health insurance.

PIP vs. MedPay (Medical Payments Coverage)

While both PIP and MedPay cover medical expenses regardless of fault, PIP is generally the superior option in Texas. MedPay only covers medical bills, whereas PIP also covers lost wages and essential services. Furthermore, MedPay often requires subrogation—meaning if you win a settlement against the at-fault driver, your auto insurer may demand to be paid back. Texas PIP does not require subrogation.

How PIP Complements Your Health Insurance

Even if you have excellent health insurance, PIP is invaluable. Health insurance often comes with high deductibles, copays, and out-of-network restrictions. PIP can be used to cover these out-of-pocket health insurance costs, ensuring you don’t go into debt just to access your medical care.

Navigating the PIP Claims Process After an Accident

To maximize your PIP benefits, you must approach the claims process systematically.

Gathering Your Medical Records and Bills

Your insurance company will not pay out simply because you state you were injured. You must provide concrete proof. Collect all medical records, diagnostic reports, and itemized billing statements related to the accident. Ensure these documents clearly link your injuries to the motor vehicle collision.

Submitting Proof of Lost Income

To claim the 80% lost wage benefit, you need two primary pieces of documentation: a doctor’s note explicitly stating you are unable to work due to your injuries, and verification of your income from your employer (such as recent pay stubs or a wage verification form).

Avoiding Delays and Denials

Insurance companies look for reasons to delay or deny claims. Avoid this by filing your PIP claim promptly, ensuring all forms are filled out accurately, and responding quickly to any requests for additional information. Do not leave gaps in your medical treatment, as insurers may argue your injuries are not as severe as claimed.

What not to say to the insurance adjuster?

When speaking to an insurance adjuster, do not say you are sorry, admit fault, or downplay your injuries by saying you feel fine. Avoid giving a recorded statement without a lawyer, and never guess or estimate facts like your speed or the exact sequence of events.

Avoiding Recorded Statements

Insurance adjusters are trained to ask leading questions that can minimize your claim. A recorded statement locks you into a narrative before you fully understand the extent of your injuries. In Texas, you are generally not required to give a recorded statement to the at-fault driver’s insurance company, and you should consult an attorney before giving one to your own.

Sticking to the Facts of the Accident

If you must speak to an adjuster to initiate your PIP claim, stick strictly to the objective facts: the date, time, location, and the fact that you are seeking medical treatment. Do not speculate about how the crash happened or offer unsolicited opinions.

How PIP Impacts Your Broader Personal Injury Claim

Filing a PIP claim does not prevent you from pursuing a liability claim against the driver who hit you. In fact, they work together.

The Collateral Source Rule in Texas

Texas follows the collateral source rule, which prevents an at-fault driver from reducing their liability just because you had the foresight to carry PIP insurance. This means you can claim the full amount of your medical bills in a lawsuit against the negligent driver, even if your PIP policy already paid those bills. Because PIP does not require subrogation, this can result in a better financial recovery for you.

Using PIP to Cover Immediate Out-of-Pocket Costs

Personal injury lawsuits can take months or years to resolve. PIP acts as a financial bridge, keeping debt collectors at bay and ensuring you can afford ongoing medical treatment while your attorney fights for your full settlement.

What not to say to a personal injury lawyer?

Never lie or withhold information from your personal injury lawyer. Do not hide pre-existing medical conditions, previous accidents, or any facts that might make you look partially at fault. Your attorney needs the complete truth to build a strong strategy and protect your claim.

The Importance of Complete Transparency

Your attorney is your advocate, and everything you discuss is protected by attorney-client privilege. If you were speeding slightly, or if you delayed going to the hospital, tell your lawyer immediately. They can handle bad facts if they know about them in advance, but surprises can destroy a case.

Why Hiding Pre-Existing Conditions Hurts Your Case

Insurance companies use sophisticated databases to track your medical history and past claims. If you hide a pre-existing back injury from your lawyer, the defense will inevitably find out and use it to attack your credibility. A skilled attorney knows how to argue that a car accident aggravated a pre-existing condition, but they can only do so if you are honest.

When to Consult a Texas Car Accident Attorney

While PIP is designed to be straightforward, insurance companies often complicate the process by delaying payouts or disputing medical necessity. Furthermore, if your damages exceed your PIP limits, you will need to navigate a third-party liability claim. Consulting with an experienced Texas personal injury attorney ensures your rights are protected, your PIP benefits are maximized, and you receive the full compensation you deserve from all available insurance policies.