Table of contents

To appeal a car insurance claim decision, first review your denial letter to understand the exact reason for rejection. Next, gather compelling evidence like police reports, photos, and witness statements. Finally, write a formal appeal letter detailing why the decision was incorrect and submit it to the claims adjuster.

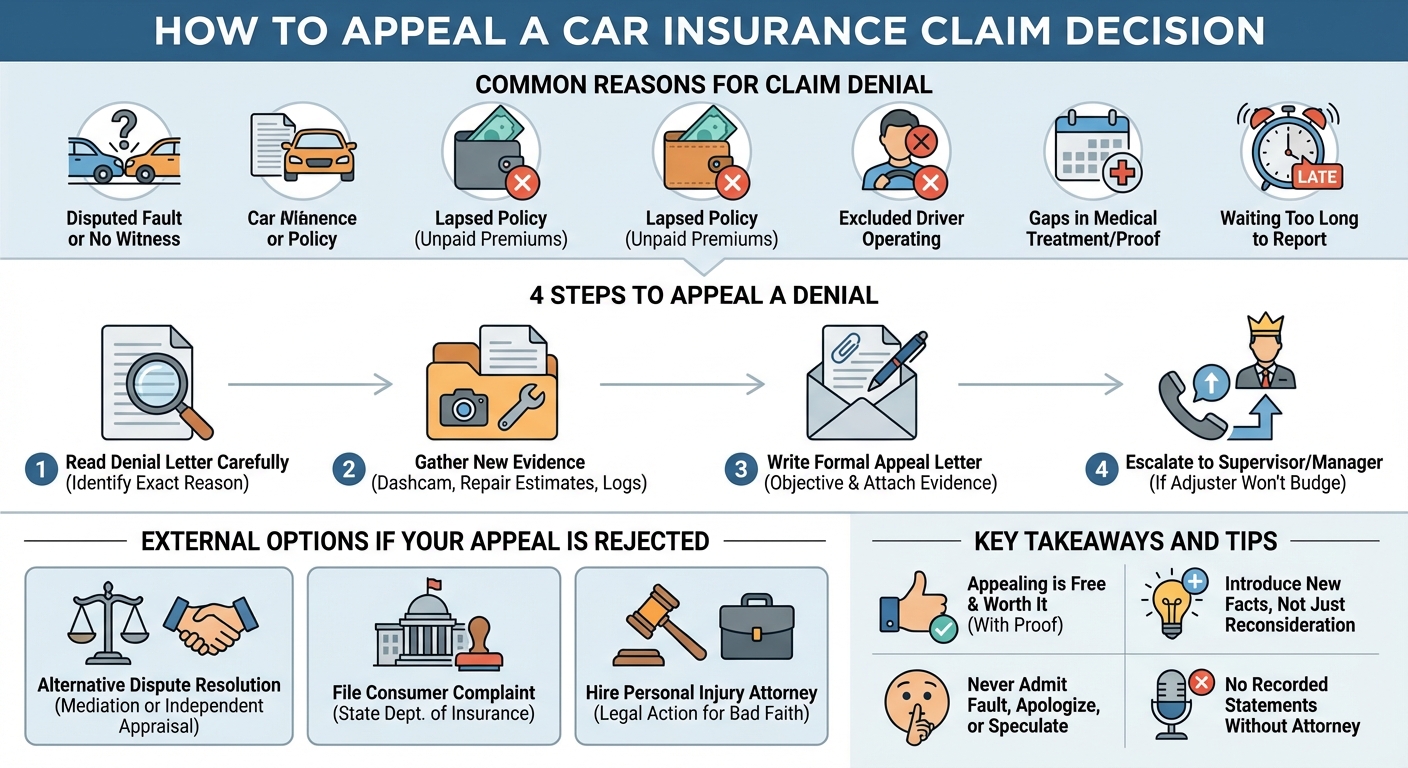

How to Appeal a Car Insurance Claim Decision: A Step-by-Step Guide

Receiving a denial letter or a lowball settlement offer from an auto insurance company can be incredibly frustrating. However, an adjuster’s initial decision is not always final. Insurance companies make mistakes, overlook critical evidence, and sometimes rely on internal algorithms that undervalue claims. If you believe your claim was unfairly denied or underpaid, you have the right to challenge it.

Appealing a car insurance claim decision requires a strategic approach. By understanding why your claim was rejected, gathering compelling evidence, and following the formal appeals process, you can successfully overturn a bad decision and secure the compensation you deserve.

Common Reasons Car Insurance Claims Are Denied

Before you can fight a denial, you must understand the insurer’s justification. Adjusters typically deny claims based on specific policy language or a perceived lack of evidence. Here are the most frequent reasons for a denied auto claim:

Disputes Over Fault or Liability

In “word vs. word” accidents where there are no independent witnesses, the insurance company may deny liability, claiming their policyholder was not at fault. If the police report is inconclusive, the insurer will almost always side with their own driver.

Lapsed Policies or Excluded Drivers

An insurer will deny coverage if the policyholder failed to pay their premiums, resulting in a lapsed policy at the time of the crash. Similarly, if the person driving the vehicle was explicitly excluded from the insurance policy, the company is not legally obligated to pay the claim.

Insufficient Medical Evidence for Injuries

If you are claiming bodily injury, insurance companies look for reasons to minimize your payout. Gaps in medical treatment, delayed doctor visits, or failing to follow a prescribed treatment plan can lead an adjuster to argue that your injuries are not serious or were pre-existing.

Delayed Reporting of the Accident

Auto insurance policies require policyholders to report accidents within a “reasonable” timeframe. If you wait weeks or months to notify the insurance company about a crash, they may deny the claim, arguing that the delay compromised their ability to investigate the incident properly.

Step-by-Step: How to Appeal a Denied Auto Insurance Claim

If your claim has been denied, do not panic. Follow these steps to build a strong appeal and force the insurance company to reconsider their position.

Step 1: Review the Denial Letter Carefully

By law, an insurance company must provide a written explanation for denying your claim. Read this letter thoroughly. Identify the specific policy exclusions or missing information the adjuster cited. Highlighting their exact reasoning gives you a clear roadmap of what you need to prove in your appeal.

Step 2: Gather New, Compelling Evidence

An appeal is rarely successful if you simply ask the adjuster to change their mind. You must introduce new facts. Depending on the reason for denial, gather the following:

- Liability disputes: Dashcam footage, surveillance video from nearby businesses, or statements from independent witnesses.

- Medical disputes: Detailed narratives from your treating physicians, MRI results, and a complete log of your medical bills.

- Property damage: Independent repair estimates from certified mechanics that contradict the insurer’s valuation.

Step 3: Write and Submit a Formal Appeal Letter

Draft a professional, concise appeal letter. Include your claim number, the date of the accident, and a direct response to the reasons listed in their denial letter. Attach your new evidence and clearly state why the initial decision was incorrect. Keep the tone objective and factual—avoid emotional language or aggressive threats.

Step 4: Escalate to a Supervisor or Claims Manager

If the original adjuster refuses to budge despite your new evidence, ask to speak with their supervisor or a claims manager. Lower-level adjusters often have strict settlement authorities and may be penalized for overturning their own denials. A supervisor has more authority to review the facts objectively and approve a payout.

What to Do If Your Auto Insurance Appeal Is Rejected

Sometimes, internal appeals hit a brick wall. If the insurance company refuses to negotiate fairly, you still have external options to pursue your claim.

Request Alternative Dispute Resolution (Mediation or Appraisal)

Many auto policies include an appraisal clause for property damage disputes. This allows you to hire an independent appraiser to assess the damage, while the insurer hires their own. If they cannot agree, a neutral umpire makes the final, binding decision. For injury claims, you may request formal mediation.

File a Complaint with the State Department of Insurance

If you believe the insurance company is violating state regulations or acting unethically, file a formal complaint with your state’s Department of Insurance. Regulatory bodies investigate consumer complaints and can pressure insurers to resolve claims if they find evidence of improper claims handling.

Consult a Personal Injury Attorney (Recognizing Bad Faith Practices)

If an insurance company unreasonably delays your claim, fails to investigate properly, or denies a clearly valid claim, they may be acting in “bad faith.” Consulting a personal injury attorney can level the playing field. An attorney can file a lawsuit, handle all communications, and hold the insurer accountable for bad faith practices.

Frequently Asked Questions About Insurance Appeals

What are the odds of winning an insurance appeal?

The odds of winning an insurance appeal depend heavily on the quality of your new evidence. If you provide clear documentation—like dashcam footage or an amended police report—your chances increase significantly. However, appealing without new facts rarely changes the adjuster’s initial decision.

Is it worth it to appeal an insurance claim?

Yes, it is absolutely worth it to appeal an insurance claim if you have evidence proving the insurer’s decision was incorrect. An appeal costs nothing to file and can result in thousands of dollars in rightful compensation for vehicle repairs, medical bills, or lost wages.

What not to say to an auto insurance adjuster?

Never admit fault, apologize, or say you are “uninjured” immediately after a crash. Avoid giving a recorded statement without legal representation, and do not speculate about how the accident happened. Stick strictly to the objective facts to prevent the adjuster from using your words against you.

What to do if insurance won’t cover Wegovy?

While this guide covers auto claims, many ask about health insurance denials like Wegovy. If denied, review your plan’s formulary requirements. Ask your prescribing doctor to submit a prior authorization appeal or a letter of medical necessity proving the medication is essential for your specific health condition.