Table of contents

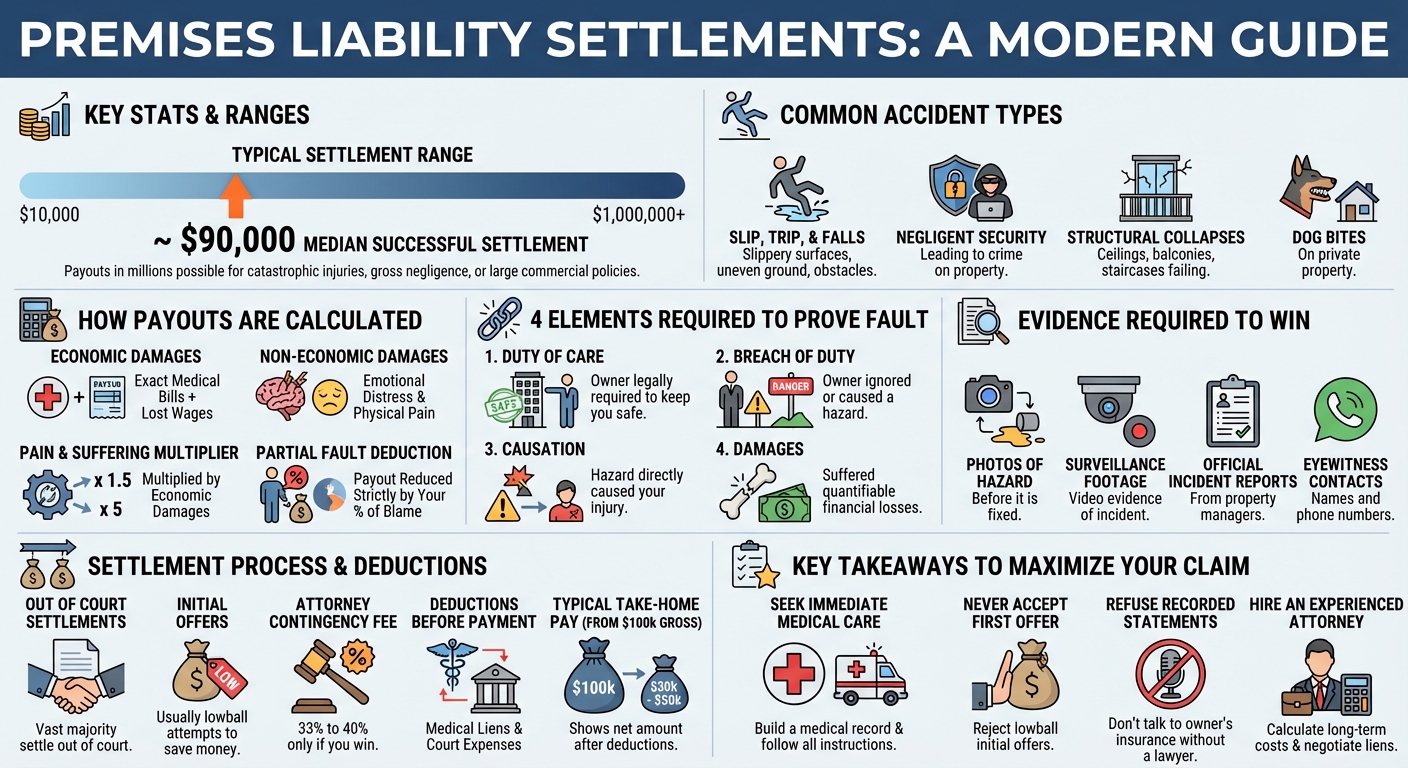

A typical premises liability settlement ranges from $10,000 to over $1 million, with the median payout around $90,000. Settlement amounts are determined by the severity of your injuries, total medical expenses, lost wages, and the degree of the property owner’s negligence.

1. Understanding Premises Liability Settlements: Average Amounts and Ranges

What is the Average Premises Liability Settlement?

Premises liability settlements in the United States vary significantly, typically ranging from $10,000 for minor injuries to over $2 million for catastrophic harm. While every case is unique, data suggests the median settlement for a successful premises liability claim hovers around $90,000. The final amount depends heavily on the severity of the injury, the clarity of fault, and the available insurance policy limits.

Factors That Push Settlements into the Millions

While average settlements fall in the five-to-six-figure range, certain factors can elevate a payout into the millions. These include:

- Catastrophic Injuries: Traumatic brain injuries (TBIs), spinal cord damage, or permanent paralysis require lifelong medical care.

- Gross Negligence: If a property owner intentionally ignored a known, severe hazard, juries and insurers are more likely to award punitive damages.

- Commercial Defendants: Corporations and large businesses carry massive commercial liability policies, providing a larger pool of available compensation compared to individual homeowners.

Common Types of Premises Liability Accidents

Premises liability is a broad legal category. Settlements are frequently negotiated for the following incident types:

- Slip, Trip, and Falls: Wet floors, uneven sidewalks, or torn carpeting.

- Negligent Security: Assaults or robberies occurring due to inadequate lighting or lack of security personnel.

- Structural Collapses: Ceiling cave-ins, balcony collapses, or broken staircases.

- Dog Bites: Animal attacks occurring on the owner’s property.

2. How Are Premises Liability Settlements Calculated?

Economic Damages: Medical Bills and Lost Wages

Economic damages form the foundation of your settlement. These are quantifiable financial losses resulting directly from the accident. They include past and future medical expenses, rehabilitation costs, and lost wages if your injury forces you to miss work. In severe cases, this also covers a loss of future earning capacity.

Non-Economic Damages: Emotional Distress

Non-economic damages compensate you for the intangible impacts of your injury. This includes emotional distress, loss of enjoyment of life, and physical pain. Because these damages lack a direct paper trail, insurance adjusters often use a multiplier method—multiplying your total economic damages by a number between 1.5 and 5—to calculate this portion of the settlement.

What is a typical amount of pain and suffering?

A typical amount for pain and suffering in a premises liability settlement is calculated using a multiplier, usually between 1.5 and 5 times your total medical bills. For minor injuries, this might mean $5,000 to $15,000, while severe, life-altering injuries can yield hundreds of thousands in non-economic damages.

How Comparative Fault Impacts Your Payout

Most states follow comparative fault or contributory negligence rules. If you are found partially responsible for your accident—for example, by texting while walking or ignoring a warning sign—your settlement will be reduced by your percentage of fault. If you are 20% at fault for a $100,000 claim, your maximum payout becomes $80,000.

3. Proving Fault: The Key to a Successful Claim

Are premises liability cases hard to win?

Premises liability cases can be hard to win because the burden of proof is entirely on the injured party. You must clearly demonstrate that the property owner knew or should have known about the hazard and failed to fix it, which often requires substantial evidence like video footage and witness testimony.

The Four Elements of Premises Liability Negligence

To secure a settlement, your legal team must prove four distinct elements:

- Duty of Care: The property owner owed you a legal duty to keep the premises safe.

- Breach of Duty: The owner failed to maintain a safe environment or warn you of hazards.

- Causation: This specific breach directly caused your injury.

- Damages: You suffered actual, quantifiable losses (medical bills, lost income) as a result.

Crucial Evidence Needed to Win Your Case

Insurance companies will look for any reason to deny your claim. Protect your settlement value by gathering robust evidence immediately after the incident. This includes taking photos of the hazard before it is fixed, securing surveillance video, filing an official incident report with the property manager, and collecting contact information from eyewitnesses.

4. The Settlement Process and Timeline

Will My Premises Liability Case Be Settled Out of Court?

Yes, the vast majority of premises liability cases are settled out of court. Trials are expensive, unpredictable, and time-consuming for both sides. Insurance companies generally prefer to negotiate a private settlement to mitigate their financial risk and avoid public verdicts.

The Insurance Company’s Initial Evaluation

Once you file a claim, the insurance adjuster will investigate the accident, review your medical records, and assess liability. They will look for inconsistencies in your story or pre-existing conditions in your medical history to devalue your claim. After their evaluation, they will typically issue an initial settlement offer.

Should I accept the first settlement offer?

You should almost never accept the first settlement offer from an insurance company. Initial offers are typically lowball figures designed to close the claim quickly and save the insurer money. Always consult with a personal injury attorney to evaluate the true, long-term value of your injuries before signing anything.

5. Understanding Your Final Payout: Fees and Deductions

How Contingency Fees Work in Personal Injury

Most premises liability attorneys work on a contingency fee basis. This means you pay no upfront costs. Instead, your lawyer takes a percentage of your final settlement—usually between 33% and 40%, depending on whether the case goes to litigation. If you do not win, you do not pay attorney fees.

Medical Liens and Out-of-Pocket Reimbursements

Before you receive your settlement check, outstanding debts related to your accident must be paid. If your health insurance, Medicare, or a hospital covered your initial treatment, they will place a medical lien on your settlement to recoup their costs. Your attorney will often negotiate these liens down to maximize your take-home amount.

How much of a $100K settlement will I get?

From a $100,000 settlement, you will typically take home between $30,000 and $50,000. This final amount is calculated after deducting your attorney’s contingency fee—usually 33% to 40%—along with case expenses, court costs, and any outstanding medical liens or health insurance reimbursements.

6. Maximizing Your Premises Liability Claim

Why Hiring an Experienced Lawyer Increases Settlement Value

Insurance companies employ teams of aggressive adjusters and lawyers to minimize payouts. Hiring a skilled personal injury attorney levels the playing field. Lawyers understand how to accurately calculate future medical costs, negotiate medical liens, and leverage the threat of a lawsuit to force higher settlement offers.

Next Steps for Your Injury Claim

If you have been injured on someone else’s property, prioritize your physical recovery first. Follow all doctor’s orders to establish a clear medical record. Then, avoid giving recorded statements to the property owner’s insurance company until you have consulted with legal counsel to protect your right to fair compensation.