Table of contents

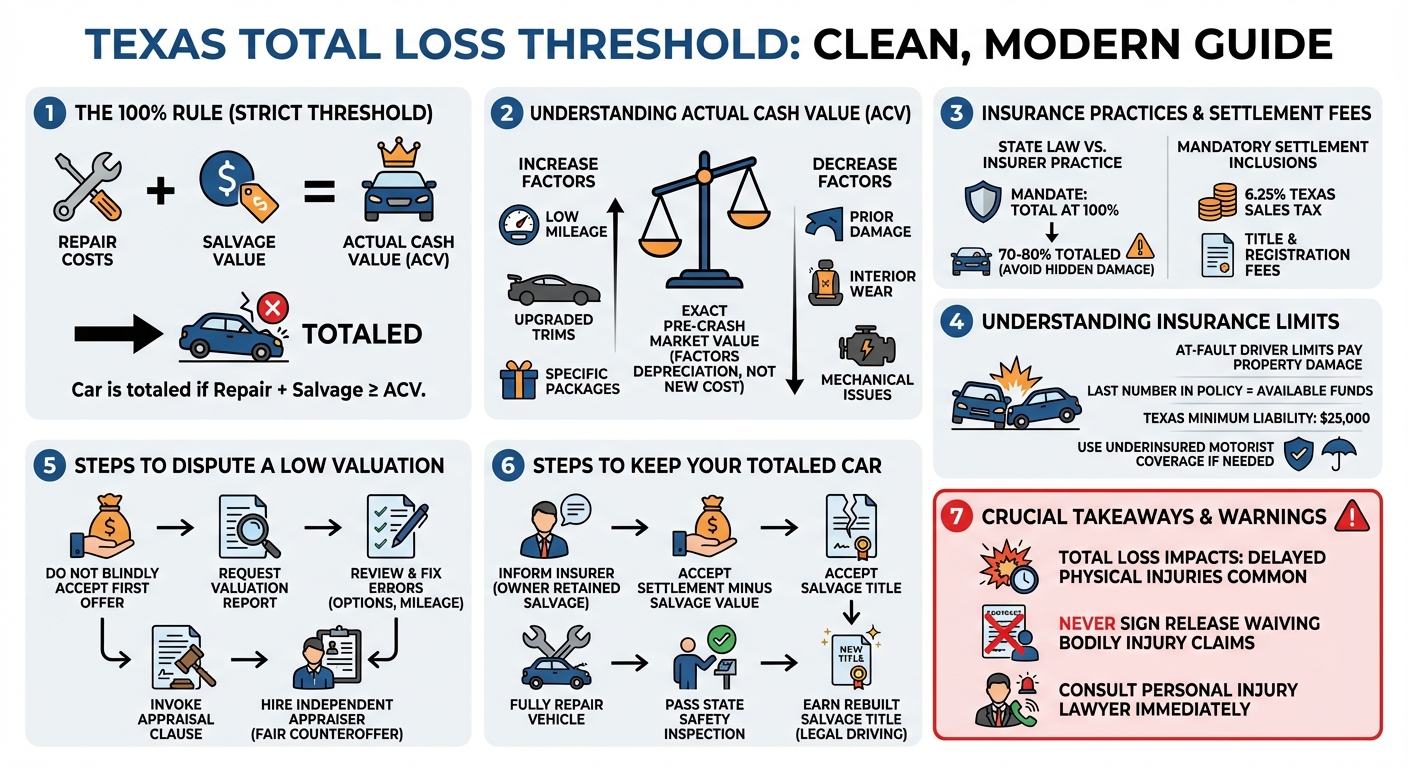

In Texas, the total loss threshold is 100%. This means an insurance company must declare your vehicle a total loss if the estimated cost of repairs plus the salvage value equals or exceeds 100% of the car’s Actual Cash Value (ACV) right before the accident.

Understanding the Texas Total Loss Threshold

After a severe car crash, dealing with the insurance company can be overwhelming. One of the most critical determinations an adjuster will make is whether your vehicle can be repaired or if it should be declared a total loss. This decision is governed by the Texas total loss threshold.

The Basics of Property Damage Claims in Texas

When another driver causes an accident in Texas, their liability insurance is responsible for your property damage. The insurer will assess your vehicle to determine the cost of repairs. If the damage is minor, they will issue a check to a body shop. However, if the structural or mechanical damage is extensive, the vehicle enters total loss territory.

Why the Threshold Matters for Your Vehicle

The total loss threshold is the legal tipping point at which an insurance company is no longer allowed to repair a vehicle. Understanding this threshold matters because it dictates whether you get your repaired car back or receive a cash settlement to purchase a replacement. Knowing the rules prevents insurers from unfairly undervaluing your settlement or forcing unsafe repairs.

What is the total loss rule in Texas?

In Texas, the total loss rule dictates a strict 100% threshold. By law, an insurance company must declare a vehicle a total loss if the estimated cost of repairs plus the vehicle’s salvage value equals or exceeds 100% of its Actual Cash Value (ACV) prior to the crash.

The 100% Total Loss Threshold Explained

While some states use a lower threshold (such as 70% or 75%), Texas uses a 100% threshold. This means a car in Texas can sustain significantly more damage and still be considered “repairable” compared to vehicles in other states. Insurers are only legally forced to total the car when the economics make repairing it completely unviable.

The Texas Total Loss Formula (TLF): Cost of Repairs + Salvage Value ≥ ACV

Texas utilizes the Total Loss Formula (TLF) to make this calculation. The formula is straightforward:

- Cost of Repairs: The body shop’s estimate to restore the car to its pre-accident condition.

- Salvage Value: What the damaged vehicle could be sold for at a scrap or salvage auction.

- Actual Cash Value (ACV): The fair market value of the car one second before the crash.

Example Calculation of a Totaled Vehicle

Imagine your car has an ACV of $15,000. After a crash, the salvage value of the wrecked car is $3,000.

If the repair estimate is $12,000, the calculation is: $12,000 (Repairs) + $3,000 (Salvage) = $15,000. Because this equals 100% of the $15,000 ACV, the vehicle must be declared a total loss.

How Insurance Companies Determine Actual Cash Value (ACV)

Factors Influencing Your Car’s ACV

Insurance companies use proprietary software (like CCC ONE) to determine your car’s ACV. They do not look at trade-in value or retail price. Instead, they evaluate:

- Mileage: Lower mileage increases ACV.

- Pre-Crash Condition: Existing dents, interior wear, or mechanical issues lower the value.

- Local Market Value: What comparable vehicles are selling for in your specific Texas zip code.

- Trim and Options: Upgraded packages, leather seats, or premium audio systems add value.

Why ACV is Lower Than Replacement Cost

Many drivers are shocked by their total loss settlement because ACV factors in depreciation. ACV is not what you originally paid for the car, nor is it the cost to buy a brand-new replacement. It is strictly the market value of your used car in its exact pre-crash state. If you have an auto loan, the ACV might even be lower than your loan balance, which is where GAP insurance becomes vital.

What is the State Farm total loss threshold in Texas?

State Farm, like all auto insurers operating in Texas, must adhere to the state’s mandatory 100% total loss threshold. However, internal guidelines may prompt them to total a vehicle earlier if hidden damages are suspected to push repair costs over the limit.

State Law vs. Internal Insurance Guidelines

While Texas law sets the ceiling at 100%, insurance companies like State Farm, GEICO, and Progressive often use internal thresholds of 70% to 80%. They do this as a financial safeguard. If an initial estimate hits 80% of the car’s value, insurers know that once a body shop begins dismantling the car, they will likely find hidden damage that pushes the cost past 100%.

Why Insurers May Total a Car Before Hitting 100% (Hidden Damages)

Modern vehicles are packed with expensive sensors, cameras, and complex crumple zones. A “teardown” frequently reveals bent frames or damaged wiring harnesses that weren’t visible on the surface. Insurers prefer to total the car early rather than paying for partial repairs only to total it weeks later.

What is the TTL amount in Texas?

In Texas, the TTL amount refers to the Tax, Title, and License fees required to register a vehicle. When your car is totaled, Texas law requires the insurance company to include the applicable state sales tax (6.25%) and standard title and registration fees in your final total loss settlement.

Defining Tax, Title, and License (TTL) Fees

When you buy a replacement vehicle, you must pay the state to legally drive it. TTL includes:

- Tax: Texas motor vehicle sales tax is 6.25%.

- Title: The fee to transfer ownership documentation.

- License: Vehicle registration fees.

Are TTL Fees Included in Your Total Loss Settlement?

Yes. The purpose of a property damage settlement is to make you “whole” again. Because you are forced to buy a replacement vehicle due to the other driver’s negligence, their insurance must compensate you for the ACV of your vehicle plus the TTL fees you will inevitably incur when purchasing a replacement.

What does 250/500/100 liability limit mean?

A 250/500/100 liability limit means an auto insurance policy covers up to $250,000 for bodily injury per person, $500,000 for total bodily injuries per accident, and $100,000 for property damage per accident. This property damage limit is what pays for your totaled vehicle if that driver is at fault.

Breaking Down the Numbers: Bodily Injury vs. Property Damage

Insurance policies are written in a three-tier format:

| Limit | Coverage Type | Explanation |

|---|---|---|

| 250 | Bodily Injury Per Person | Pays up to $250,000 for medical bills and pain/suffering for a single injured person. |

| 500 | Bodily Injury Per Accident | Pays up to $500,000 total for all injured people in the crash combined. |

| 100 | Property Damage | Pays up to $100,000 to repair or replace vehicles and property damaged by the insured. |

How the $100,000 Property Damage Limit Applies to Your Totaled Car

If the at-fault driver has a 250/500/100 policy, there is $100,000 available to cover your totaled vehicle. If your car’s ACV is $45,000, this limit is more than enough to fully compensate you.

What Happens if the At-Fault Driver’s Limits Are Too Low?

The Texas state minimum for property damage is only $25,000. If your totaled vehicle is worth $60,000 and the at-fault driver only carries state minimums, their insurance will only pay $25,000. To recover the rest, you would need to file a claim under your own Underinsured Motorist Property Damage (UMPD) or Collision coverage.

What to Do If You Disagree With the Insurance Company’s Valuation

Requesting the Insurer’s Valuation Report

Never accept the first settlement offer blindly. Ask the adjuster for the comprehensive valuation report (often a CCC ONE report). Review it carefully. Insurers frequently make mistakes, such as listing your car as a base model when it is a premium trim, or inaccurately recording the mileage.

Invoking the Appraisal Clause

If you are using your own collision coverage and cannot agree on the ACV, you can invoke the “Appraisal Clause” in your policy. This allows both you and the insurer to hire independent appraisers. If the two appraisers cannot agree, an impartial umpire makes the final, binding decision.

Hiring an Independent Auto Appraiser

Even if you are dealing with the at-fault driver’s insurance, hiring an independent appraiser can provide you with a well-documented counteroffer. An independent appraiser will pull local comps and accurately assess your vehicle’s pre-crash condition to fight back against lowball offers.

Can You Keep a Totaled Car in Texas?

Owner-Retained Salvage Rules

Yes, Texas allows you to keep a totaled vehicle. This is known as an “owner-retained salvage.” If you have a sentimental attachment to the car or believe you can repair it cheaply yourself, you have the right to keep it.

Getting a Salvage Title in Texas

If you keep a totaled car, the insurance company will notify the Texas Department of Motor Vehicles (TxDMV). Your clean title will be replaced with a Salvage Title. You cannot legally drive a salvage vehicle on public roads until it has been fully repaired, passes a strict safety inspection, and is issued a Rebuilt Salvage Title.

Deductions from Your Settlement Payout

If you choose to keep the car, the insurance company will deduct the vehicle’s salvage value from your settlement. For example, if your ACV is $10,000 and the salvage value is $2,000, the insurer will write you a check for $8,000 and let you keep the damaged car.

Property Damage vs. Personal Injury: Protecting Your Entire Claim

Why a Totaled Car Often Means Severe Physical Injuries

The forces required to total a modern vehicle are immense. If your car sustained enough structural damage to meet the 100% Texas total loss threshold, your body absorbed a massive amount of kinetic energy. Injuries like whiplash, concussions, or spinal disc damage may not manifest fully until days after the crash. Never sign a release of liability for your property damage if it includes language releasing your bodily injury claims.

When to Consult a Texas Car Accident Lawyer

While you can often handle a straightforward property damage claim on your own, you should consult a Texas personal injury lawyer immediately if you suffered physical injuries. Insurance companies often use property damage settlements to quickly close out a claim before the victim realizes the true extent of their medical needs. An attorney will ensure your medical records are properly documented and fight to maximize both your property and injury compensation.