Table of contents

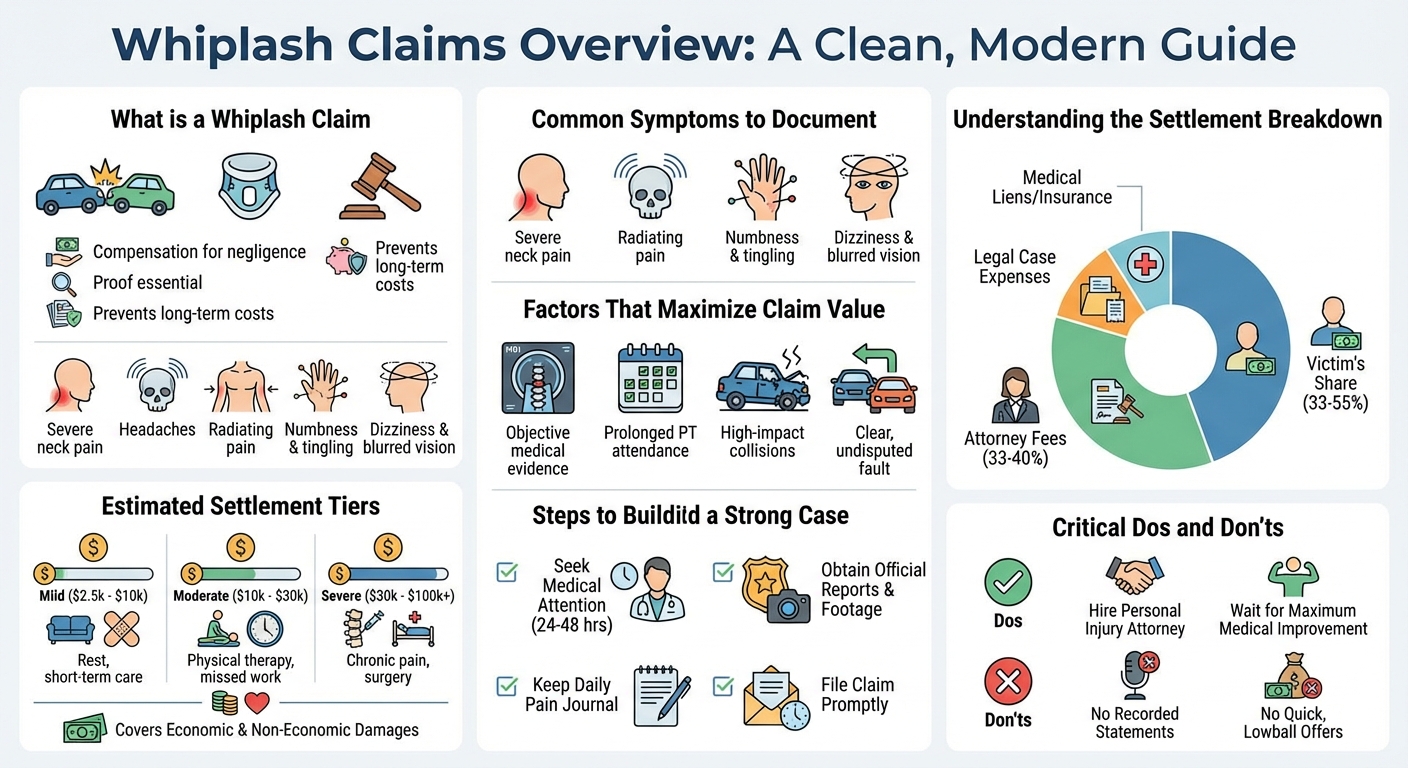

A whiplash claim is a personal injury case filed to seek compensation for neck injuries sustained in an accident. Successful whiplash claims typically result in settlements ranging from $10,000 to $30,000, covering medical bills, lost wages, and pain and suffering caused by the at-fault party’s negligence.

Understanding Whiplash Claims After a Car Accident

Whiplash is one of the most common injuries sustained in rear-end collisions, yet it is also one of the most misunderstood. Filing a whiplash claim allows victims to recover financial compensation for the physical and financial toll of the injury.

What constitutes a valid whiplash claim?

A valid whiplash claim requires proving that another party’s negligence caused your injury. You must show that the at-fault driver breached their duty of care (e.g., by texting and driving or tailgating), which directly resulted in the accident and your subsequent neck injury. Documented medical evidence linking the crash to your diagnosis is the foundation of a strong claim.

Why insurance companies fight whiplash claims (Debunking the fake injury myth)

Insurance adjusters are notoriously skeptical of soft tissue injuries. Because whiplash involves damage to muscles, ligaments, and tendons rather than easily visible bone fractures, insurers often try to downplay the severity of the injury. They rely on the outdated myth that whiplash claims are exaggerated or “fake” to justify lowball settlement offers or outright denials.

Common symptoms that validate your injury claim

To overcome insurance skepticism, prompt medical documentation of your symptoms is critical. Common signs of whiplash include:

- Severe neck pain and stiffness

- Headaches starting at the base of the skull

- Pain radiating into the shoulders, upper back, or arms

- Numbness or tingling in the arms

- Dizziness and blurred vision

How much would you get in a claim for whiplash?

The amount you get in a whiplash claim typically ranges from $2,500 for mild cases to over $30,000 for severe injuries. Your total compensation depends on your specific economic damages, such as medical bills and lost wages, plus non-economic damages for pain, suffering, and loss of mobility.

Compensation tiers: Mild, moderate, and severe whiplash

Settlement values generally fall into three tiers based on the severity and duration of the injury:

| Injury Severity | Estimated Settlement Range | Typical Treatment Required |

|---|---|---|

| Mild | $2,500 – $10,000 | Rest, pain medication, short-term chiropractic care. Resolves in weeks. |

| Moderate | $10,000 – $30,000 | Extensive physical therapy, prescription medications, missed work. Lasts months. |

| Severe | $30,000 – $100,000+ | Injections, potential surgery, chronic pain management, permanent impairment. |

Economic damages: Medical bills and lost wages

Economic damages reimburse you for out-of-pocket losses. This includes emergency room visits, diagnostic imaging (X-rays, MRIs), physical therapy sessions, and prescription costs. It also covers lost wages if your injury forced you to miss work or use paid time off.

Non-economic damages: Pain, suffering, and loss of mobility

Non-economic damages compensate you for the subjective impact of the injury. If whiplash prevents you from picking up your children, participating in hobbies, or causes chronic sleep disruption due to pain, these factors significantly increase the value of your claim.

What is the average payout for whiplash?

The average payout for a standard whiplash injury in a car accident is generally between $10,000 and $30,000. However, this average can fluctuate significantly based on the severity of the collision, the duration of your medical treatment, and the at-fault driver’s insurance policy limits.

Factors that increase your settlement value

Several variables can push a whiplash settlement above the average mark:

- Objective medical evidence: MRIs showing torn ligaments or herniated discs.

- Prolonged treatment: Consistent attendance at months of physical therapy.

- High-impact collisions: Severe vehicle damage that corroborates the force of the impact.

- Clear liability: Undisputed evidence (like dashcam footage) proving the other driver was 100% at fault.

Why average numbers can be misleading for your specific case

Relying on “average” settlement calculators can be dangerous. Every case is unique. If the at-fault driver only carries state-minimum liability insurance, your payout might be capped regardless of your damages, unless you have Underinsured Motorist (UIM) coverage. Conversely, if a commercial vehicle caused your whiplash, the available policy limits—and your potential payout—could be much higher.

How much of a $100K settlement will I get?

From a $100,000 settlement, you will typically receive between $33,000 and $55,000 in your pocket. This final net payout is calculated after deducting standard attorney contingency fees (usually 33% to 40%), legal case expenses, and reimbursing any medical liens or health insurance subrogation claims.

Understanding the breakdown of a personal injury settlement

A settlement check does not go entirely to the victim. The funds must first be distributed to cover the costs of securing the settlement and treating the injury. Understanding this breakdown prevents surprises when your case concludes.

Deducting attorney contingency fees and legal expenses

Most personal injury lawyers work on a contingency fee basis, meaning they take a percentage of the settlement (typically 33.3% if settled before litigation, or 40% if a lawsuit is filed). Additionally, case expenses—such as fees for obtaining medical records, hiring expert witnesses, and court filing costs—are deducted from the gross amount.

Paying off medical liens and health insurance subrogation

If your health insurance, Medicare, or a hospital paid for your whiplash treatment upfront, they have a legal right to be reimbursed from your settlement. Your attorney will negotiate these medical liens down as much as possible to maximize your take-home amount.

Calculating your final net payout

Here is a simplified example of a $100,000 settlement breakdown:

- Gross Settlement: $100,000

- Attorney Fees (33.3%): -$33,333

- Case Expenses: -$2,500

- Medical Liens: -$15,000

- Your Net Payout: $49,167

Is it worth claiming whiplash?

Yes, claiming whiplash is absolutely worth it. Ignoring a neck injury can leave you financially responsible for hidden long-term medical costs, chronic pain management, and missed work. Filing a claim ensures the at-fault party’s insurance covers your treatment and compensates you for your suffering.

The hidden long-term costs of ignoring neck injuries

What feels like minor stiffness on the day of the crash can evolve into chronic pain, debilitating migraines, and early-onset spinal osteoarthritis. If you settle too early or fail to file a claim, you will have to pay for future chiropractic care, physical therapy, or pain injections out of your own pocket.

Secondary complications

Whiplash does not just affect the neck. The violent back-and-forth motion of a crash can cause severe trauma to the jaw. In fact, TMJ injuries from car accidents are an overlooked consequence of whiplash. Treating secondary complications like Temporomandibular Joint disorders requires specialized dental care, which should be fully covered by your injury claim.

Protecting your legal rights before the statute of limitations expires

Every state has a strict deadline, known as the statute of limitations, for filing a personal injury lawsuit. If you wait to see if your whiplash “gets better on its own” and miss this deadline, you permanently lose your right to seek compensation. Initiating a claim immediately protects your legal options.

Evidence Needed for a Successful Whiplash Claim

Because whiplash is an “invisible” injury, your claim is only as strong as your evidence. Building a watertight case requires swift action.

The importance of immediate medical attention and imaging (X-rays, MRIs)

See a doctor within 24 to 48 hours of your accident. While X-rays will not show soft tissue damage, they rule out fractures. More importantly, an MRI can reveal micro-tears in ligaments, muscle damage, and herniated discs, providing the objective proof insurance adjusters demand.

Gathering police reports, dashcam footage, and witness statements

Liability must be clearly established. Obtain the official police crash report, which often indicates who was at fault. If available, secure dashcam footage, traffic camera recordings, and contact information for eyewitnesses who can testify to the severity of the impact.

Keeping a daily pain journal to document your recovery

Non-economic damages are hard to quantify. Keeping a daily journal detailing your pain levels, the medications you take, and the daily activities you are forced to miss (like picking up your child or exercising) provides compelling evidence of how the whiplash has impacted your quality of life.

Dos and Don’ts When Dealing with Insurance Adjusters

Insurance adjusters are trained negotiators whose primary goal is to minimize the company’s financial exposure. Protect your claim by following these critical rules.

Why you should never give a recorded statement without a lawyer

Don’t: Agree to a recorded statement with the at-fault driver’s insurance company. Adjusters will ask leading questions designed to make you admit fault or downplay your injuries (e.g., “You’re feeling a little better today, right?”).

Do: Direct all communication to your personal injury attorney.

Avoiding early lowball settlement offers

Insurers often dangle quick, low-dollar settlement checks within days of the accident, hoping you will accept before you realize the full extent of your whiplash. Once you sign a release and accept the money, your case is closed forever. Never accept an offer until you have reached Maximum Medical Improvement (MMI).

How a personal injury attorney maximizes your whiplash compensation

A skilled attorney levels the playing field. They will handle all adjuster communications, gather critical medical evidence, negotiate down your medical liens, and aggressively push for a settlement that reflects the true value of your economic and non-economic damages. If the insurance company refuses to offer a fair amount, your lawyer will be prepared to take your whiplash claim to court.