Table of contents

To collect PIP insurance, seek medical treatment immediately after your accident to document your injuries. Next, notify your auto insurance provider and request a PIP application. Fill out the application completely, submit it with your medical records, and have your healthcare providers bill your auto insurer directly.

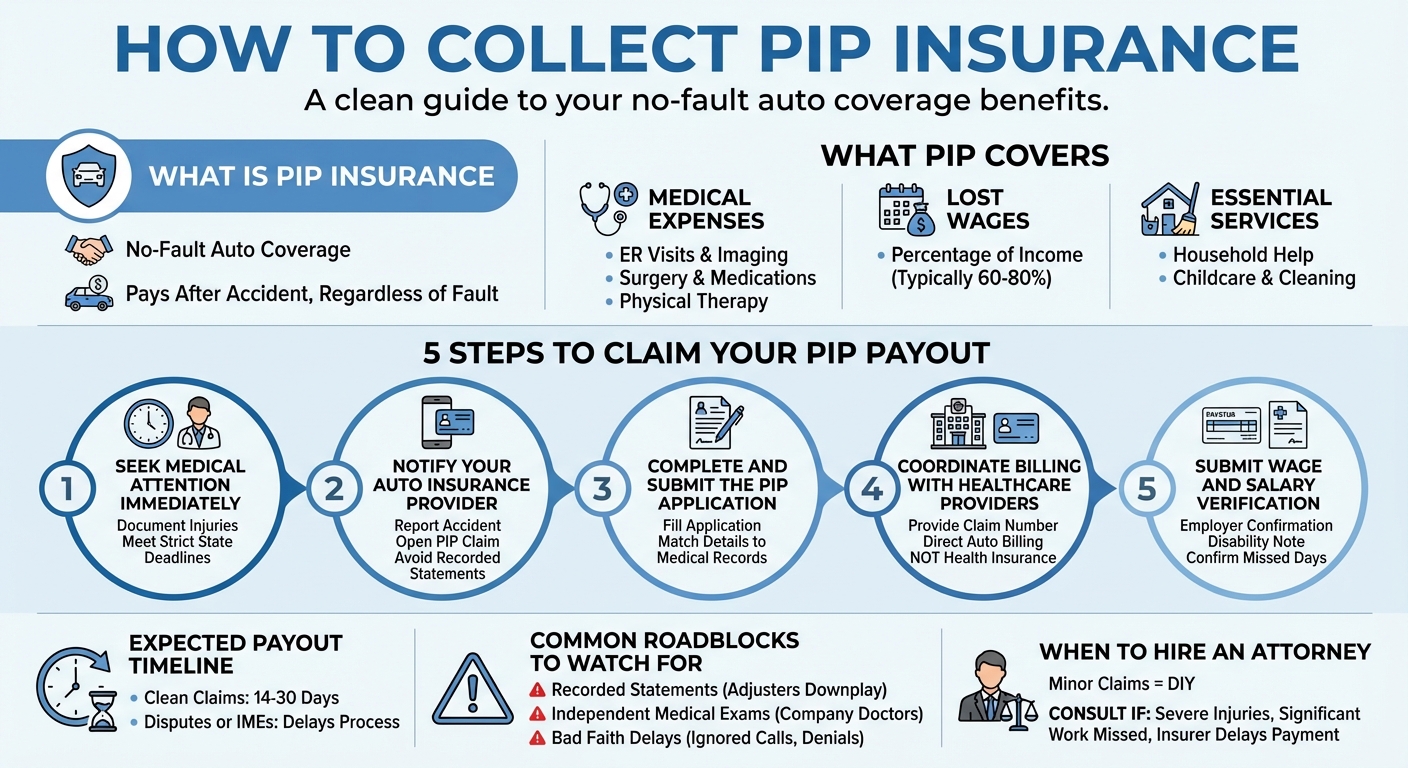

How to Collect PIP Insurance: A Step-by-Step Guide to Getting Your Payout

If you have been injured in a car accident, Personal Injury Protection (PIP) is designed to be your first line of financial defense. Because PIP is “no-fault” coverage, you do not have to prove the other driver caused the crash to access your benefits. However, insurance companies still require strict adherence to their claims process before releasing any funds.

Understanding exactly how to collect PIP insurance ensures your medical bills are paid promptly and your lost wages are recovered while you heal. Below is a comprehensive guide to navigating the PIP claims process.

What is a PIP payout?

A PIP payout is a financial reimbursement from your auto insurance company under your Personal Injury Protection coverage. It compensates you for medical bills, lost wages, and essential out-of-pocket expenses after a car accident, regardless of who was at fault for the crash.

What does PIP insurance pay for?

PIP insurance pays for reasonable and necessary medical expenses, such as hospital visits, surgeries, and physical therapy. Additionally, it covers a percentage of your lost wages if you cannot work, and reimburses you for essential services like childcare or house cleaning while you recover.

Medical Expenses Covered by PIP

Your PIP coverage typically handles the immediate and ongoing medical costs associated with your accident. This includes:

- Ambulance rides and emergency room visits

- Diagnostic imaging (X-rays, MRIs)

- Surgical procedures and hospital stays

- Prescription medications

- Rehabilitation and physical therapy

Lost Wages and Income Replacement

If your injuries prevent you from returning to work, PIP acts as a partial income replacement. Most policies cover a specific percentage of your gross income (often between 60% and 80%), up to your policy’s maximum limit. You will need your employer to verify your absence and standard pay rate to collect this benefit.

Essential Services and Out-of-Pocket Costs

Severe injuries can make daily household tasks impossible. PIP can reimburse you for “replacement services.” If you have to hire someone to mow your lawn, clean your house, or care for your children while you are incapacitated, these out-of-pocket expenses are often covered under your policy.

How do I claim for PIP?

To claim for PIP, you must first seek immediate medical attention for your injuries. Next, notify your auto insurance provider about the accident and request a PIP application. Complete and submit this form promptly, then coordinate with your healthcare providers to send medical bills directly to your insurer.

Step 1: Seek Medical Attention Immediately (Mind the Deadlines)

Insurance companies look for any reason to deny a claim, and a delay in medical treatment is their favorite excuse. Many states have strict deadlines—such as the 14-day rule in Florida—meaning if you do not see a doctor within that window, you forfeit your PIP benefits entirely. Always get checked out immediately, even if you feel fine at the scene.

Step 2: Notify Your Auto Insurance Provider

Call your insurance agent or use your provider’s mobile app to report the accident. Inform them that you were injured and intend to open a PIP claim. Do not discuss fault or give a recorded statement at this stage; simply provide the basic facts of the crash (date, time, location).

Step 3: Complete and Submit the PIP Application

Your insurer will send you a formal PIP application (sometimes called an Application for Benefits). Fill this out accurately and return it as soon as possible. This document officially triggers your coverage. Ensure all personal details, accident descriptions, and listed injuries are consistent with your medical records.

Step 4: Coordinate Billing with Your Healthcare Providers

Give your auto insurance claim number and your adjuster’s contact information to your doctors, hospitals, and physical therapists. Instruct them to bill your auto insurance (PIP) directly, rather than your standard health insurance. This prevents you from paying out-of-pocket deductibles upfront.

Step 5: Submit Your Wage and Salary Verification Form

If you are claiming lost wages, you must submit a Wage and Salary Verification form. Your employer will need to fill out their portion to confirm your pay rate and the days you missed. Your doctor must also provide a disability note stating that your injuries medically required you to stay home from work.

How long does a personal injury claim take to pay out?

A personal injury claim under PIP typically takes 14 to 30 days to pay out once the insurance company receives your completed application and medical bills. However, if the insurer disputes your treatment or requests an independent medical exam, the payout process can be significantly delayed.

Common Roadblocks When Collecting PIP Benefits

Even though PIP is your own coverage, your insurance company is still a for-profit business. They may employ tactics to minimize or delay your payout.

The Recorded Statement Trap

Adjusters often ask for a recorded statement under the guise of “processing your claim faster.” In reality, they are looking for inconsistencies in your story or trying to get you to downplay your injuries. You are generally required to cooperate with your own insurer, but you should consult an attorney before providing a formal recorded statement.

Independent Medical Examinations (IMEs)

If your medical treatment extends for a long period, your insurer may demand you attend an Independent Medical Examination (IME). This doctor is hired by the insurance company to evaluate whether you still need treatment. Often, IME doctors will claim you are fully healed, giving the insurer an excuse to cut off your PIP benefits.

Bad Faith Delays and Denials

Sometimes, insurance companies engage in bad faith practices. This includes ignoring your calls, losing your paperwork, or denying valid medical bills without a reasonable explanation. If your own insurance company is working against you, it may be time to escalate the situation.

Do You Need an Attorney to Collect PIP?

For minor accidents with a single emergency room visit, you can usually collect PIP insurance on your own by following the steps above. However, if your injuries are severe, you are missing significant time from work, or your insurance adjuster is delaying your payments, consulting a personal injury attorney is highly recommended. A lawyer can force the insurance company to honor their policy, handle the billing coordination, and protect you from bad faith tactics.