Table of contents

If you are being sued for a car accident, immediately notify your auto insurance company. Your insurer has a legal duty to defend you and will typically hire an attorney to handle the lawsuit on your behalf.

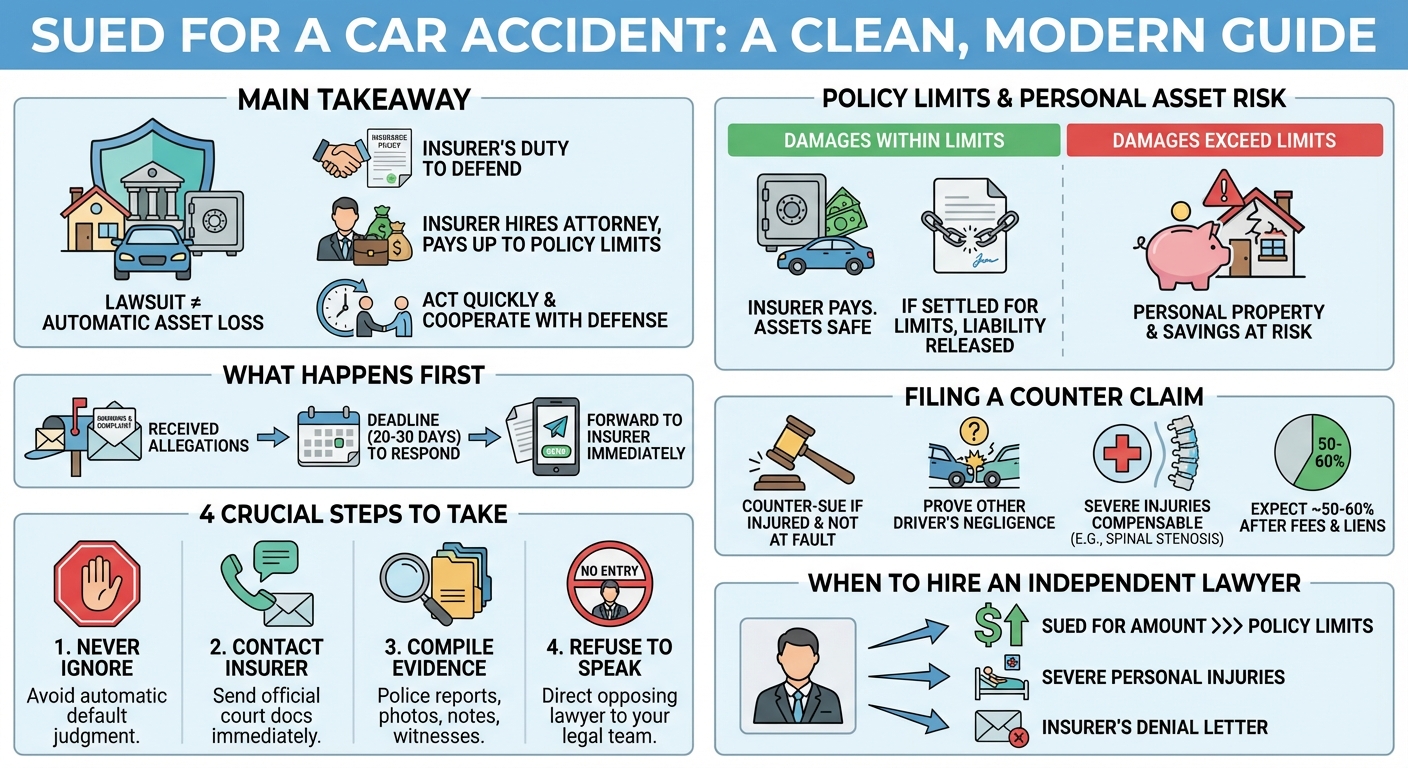

I Am Being Sued for a Car Accident: Immediate Steps and Legal Rights

Finding out you are being sued for a car accident can be incredibly stressful. Whether the crash happened weeks or months ago, receiving formal legal documents in the mail or via a process server is an intimidating experience. However, it is important to remember that being sued does not automatically mean you will lose your personal assets.

In most cases, your auto insurance policy includes a “duty to defend” clause. This means your insurance provider is legally obligated to hire an attorney to represent you and pay for damages up to your policy limits. The key to protecting yourself is acting quickly, understanding your legal rights, and cooperating fully with your defense team.

What happens if someone sues me for a car accident?

If someone sues you for a car accident, you will receive a formal summons and complaint. You must immediately forward these documents to your auto insurance company. Your insurer will then assign a defense attorney to represent you and cover any resulting damages up to your policy limits.

Receiving the Summons and Complaint

A lawsuit officially begins when you are served with a “Summons and Complaint.” The Complaint outlines the plaintiff’s allegations against you, detailing how they believe you caused the accident and the specific damages they are seeking (such as medical bills, lost wages, and pain and suffering). The Summons is a court document notifying you of your deadline to file a formal response.

Your Auto Insurance Company’s Duty to Defend

When you purchase auto insurance, you are buying more than just financial coverage; you are buying legal protection. Your insurance company has a contractual “duty to defend” you in court. Once notified, they will appoint and pay for an insurance defense attorney to handle the litigation, file the necessary court responses, and attempt to negotiate a settlement on your behalf.

4 Crucial Steps to Take After Being Served

1. Never Ignore the Lawsuit (Avoid Default Judgments)

The worst mistake you can make is ignoring the lawsuit. You typically have a strict deadline (often 20 to 30 days, depending on your state) to file a formal answer with the court. If you fail to respond, the judge may issue a default judgment against you, meaning the plaintiff automatically wins and can begin collecting money directly from your personal assets.

2. Contact Your Auto Insurance Provider Immediately

Call your insurance adjuster the moment you are served. Follow up by sending them a copy of the Summons and Complaint via certified mail or a tracked email portal. Your insurer cannot defend you if they do not know the lawsuit exists.

3. Compile All Accident Documentation and Police Reports

Gather every piece of evidence you have regarding the crash. This will help your assigned defense attorney build a strong case. Essential documents include:

- The official police report

- Photographs of the accident scene and vehicle damage

- Contact information for any eyewitnesses

- Your personal notes detailing how the crash occurred

4. Do Not Communicate with the Plaintiff’s Lawyer

Once a lawsuit is filed, all communication must go through your legal representation. If the plaintiff’s attorney contacts you, politely decline to speak with them and direct them to your insurance company or assigned defense lawyer. Anything you say can be used against you to establish liability.

What Happens If You Are Sued for More Than Your Liability Coverage?

Understanding Your Policy Limits

Your insurance company will only pay damages up to the maximum limit of your liability coverage. For example, if you have $50,000 in bodily injury coverage and the jury awards the plaintiff $75,000, there is a $25,000 shortfall. This excess amount is technically your personal responsibility.

Protecting Your Personal Assets from Excess Judgments

If the plaintiff is seeking damages that exceed your policy limits, you may be personally exposed. Here is a breakdown of how different scenarios are typically handled:

| Scenario | Who Pays the Damages? | Risk to Personal Assets |

|---|---|---|

| Damages are within policy limits | Your auto insurance provider | None. The insurer covers the full settlement. |

| Damages exceed policy limits | Insurer pays up to the limit; you owe the rest | High. Plaintiff can pursue your savings or property. |

| Plaintiff settles for policy limits | Your auto insurance provider | None. Plaintiff signs a release of liability. |

In many cases, plaintiffs will agree to settle for the policy limits rather than pursue a lengthy battle for personal assets, especially if the defendant does not have significant wealth.

Understanding Accident Claims: Injuries and Compensation

Can a car accident cause spinal stenosis?

Yes, a car accident can cause or aggravate spinal stenosis. The severe physical impact of a crash can narrow the spinal canal, compress surrounding nerves, or worsen pre-existing spinal conditions, leading to chronic pain, numbness, and the need for extensive medical treatment.

What is the average compensation for a car accident?

There is no single average compensation for a car accident, as settlements vary widely based on injury severity, liability, and insurance limits. Minor crashes may settle for a few thousand dollars, while severe injury cases can result in six- or seven-figure payouts.

Filing a Counter-Claim: What If You Were Also Injured?

If you believe the other driver was actually at fault—or partially at fault—and you suffered injuries, you have the right to file a counter-claim. You do not have to simply play defense; you can seek compensation for your own medical bills and property damage.

Proving the Other Driver Was at Fault

To succeed in a counter-claim, you must prove the plaintiff’s negligence contributed to the crash. This requires leveraging evidence like dashcam footage, skid mark analysis, and witness testimony. If you live in a comparative negligence state, you can still recover damages even if you were partially at fault, though your compensation will be reduced by your percentage of blame.

How much of a $100K settlement will I get?

If you secure a $100,000 settlement from a counter-claim, you will typically receive between $50,000 and $60,000. This is because standard contingency attorney fees take about 33%, and the remaining funds must cover outstanding medical liens, court costs, and case expenses.

When to Consult an Independent Personal Injury Lawyer

While your insurance company will provide a lawyer to defend you, that attorney’s primary goal is to protect the insurance company’s bottom line. You should consider consulting an independent personal injury lawyer if:

- You are being sued for an amount significantly higher than your policy limits.

- You suffered severe injuries in the crash and need to file a counter-claim.

- Your insurance company is issuing a “Reservation of Rights” letter, indicating they may deny coverage for the claim.

An independent attorney works solely for you, ensuring your personal assets are protected and your own injury claims are aggressively pursued.