Table of contents

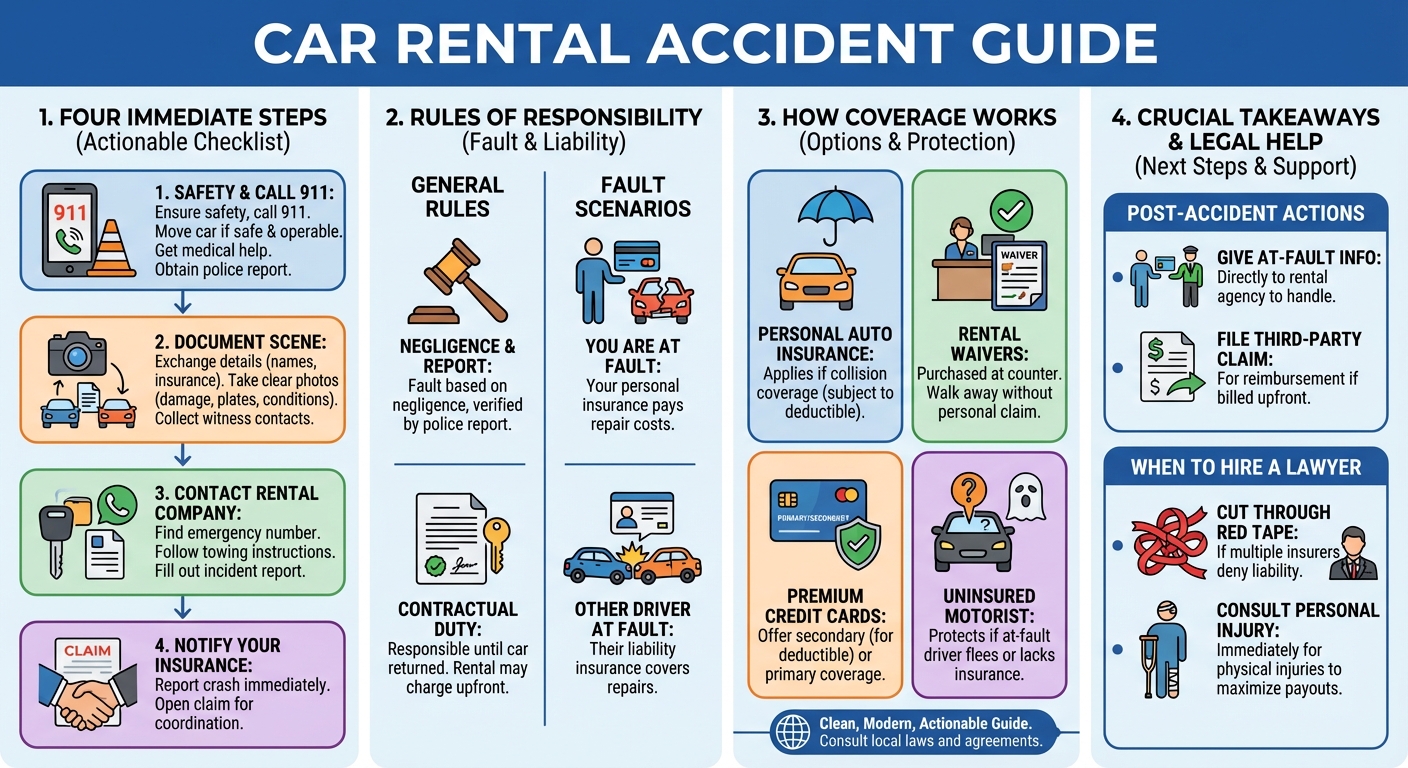

If you get into a car rental accident, first ensure everyone’s safety and call 911. Next, document the scene and exchange information. You must then notify the rental car company to file an incident report, followed by your personal auto insurance provider, who typically covers rental damages if you have collision coverage.

What to Do Immediately After a Car Rental Accident

Getting into a crash is always stressful, but a car rental accident adds an extra layer of complexity. You are dealing with a vehicle you don’t own, a rental contract, and potentially multiple insurance policies. Taking the right steps immediately can protect you from massive out-of-pocket costs.

1. Ensure Safety and Call 911

Your first priority is health and safety. Move the rental vehicle to the side of the road if it is safe and operable. Call 911 immediately to request medical assistance if anyone is injured and to ensure police arrive to draft an official accident report. A police report is vital for both the rental agency and insurance claims.

2. Exchange Information and Document the Scene

Gather as much evidence as possible while at the scene. This protects you against false claims later.

- Driver details: Get the names, contact info, driver’s license numbers, and insurance details of all involved parties.

- Photographic evidence: Take clear photos of the damage to all vehicles, the rental car’s license plate, skid marks, and overall road conditions.

- Witnesses: Collect names and phone numbers of anyone who saw the crash.

3. Contact the Rental Car Company

Check your rental agreement or the sticker inside the glovebox for the rental company’s emergency contact number. You must notify them of the accident as soon as possible. They will instruct you on where to tow the vehicle if it is undrivable and require you to fill out an official incident report.

4. Notify Your Personal Auto Insurance Provider

Even if you purchased coverage at the rental counter, you should report the accident to your personal auto insurance provider. Prompt reporting ensures they can open a claim, investigate the facts, and coordinate with the rental company if your personal policy needs to cover the damages.

Who is responsible for a rental car in an accident?

The person responsible for a rental car in an accident depends on who caused the crash. If you are at fault, you (or your insurance) are responsible for the damages. If another driver caused the crash, their liability insurance is responsible for covering the rental car’s repair costs.

Determining Fault in a Rental Collision

Fault is determined exactly as it is in a standard car crash—based on negligence. Insurance adjusters and law enforcement will review the police report, physical evidence, and witness statements to decide who violated traffic laws or failed to drive safely.

The Renter’s Contractual Obligations

When you sign a rental agreement, you assume financial responsibility for the vehicle until it is returned. Even if another driver is at fault, the rental company may initially charge your credit card for the damages. You or your insurance company will then need to seek reimbursement from the at-fault party’s insurer.

Will my insurance cover a rental accident?

Yes, in most cases, your personal auto insurance will cover a rental accident if you carry comprehensive and collision coverage. Your policy limits and deductibles will apply exactly as they would for your own vehicle, covering damages to the rental car and liability for other parties.

How Personal Auto Insurance Applies to Rentals

Personal auto policies typically “follow the driver, not the car.” This means your liability coverage pays for damage you cause to others, while your collision coverage pays for damage to the rental car. You will still be responsible for paying your standard deductible.

Understanding Collision Damage Waivers (CDW) and Loss Damage Waivers (LDW)

At the rental counter, you are often pitched a CDW or LDW. These are not technically insurance; they are waivers stating the rental company will not hold you financially responsible if the car is damaged or stolen. If you purchased this waiver, you can generally return the damaged car and walk away without filing a claim on your personal insurance, provided you didn’t violate the rental agreement (e.g., driving under the influence).

Credit Card Rental Car Insurance Benefits

Many premium credit cards offer rental car insurance if you used the card to pay for the rental.

- Secondary Coverage: Most cards offer secondary coverage, meaning they pay your personal insurance deductible and fees your insurer won’t cover.

- Primary Coverage: A few premium cards offer primary coverage, allowing you to bypass your personal auto insurance entirely for vehicle damage.

What if someone crashes your rental car?

If someone crashes into your rental car and they are at fault, their auto insurance is responsible for paying the damages. You must still notify the rental company and file an incident report, but the at-fault driver’s property damage liability coverage will ultimately cover the repair costs.

When Another Driver is at Fault

Treat the situation like any other accident. Ensure the police document the other driver’s fault in their report. Provide the at-fault driver’s insurance information directly to the rental agency so they can pursue the claim.

Filing a Claim Against the At-Fault Driver’s Insurance

The rental company’s damage recovery unit will usually deal directly with the at-fault driver’s insurance company. However, if the rental agency charges your card for the damage upfront, you will need to file a third-party claim with the at-fault driver’s insurer to get reimbursed.

Dealing with Uninsured Motorists in a Rental

If the at-fault driver is uninsured or flees the scene, you will have to rely on your own Uninsured Motorist (UM) coverage, your credit card benefits, or the rental company’s LDW if you purchased it. Otherwise, you may be held personally liable for the repairs.

Navigating Rental Reimbursement and Replacement Vehicles

How Rental Reimbursement Coverage Works

If you are driving a rental because your personal car was in an accident, your policy’s “rental reimbursement coverage” pays for the daily rate of the rental car up to a specific limit (e.g., $30 per day for 30 days). If you get into an accident in this replacement vehicle, the same insurance rules apply as a standard rental.

Can an insurance company just give you money to get a rental car yourself?

Yes, an insurance company can just give you money to get a rental car yourself. This is known as a “cash out” option. Instead of the insurer paying the rental agency directly, they issue you a check for the daily rental allowance multiplied by the estimated repair days.

When to Hire a Lawyer for a Rental Car Accident

Handling Complex Liability and Multiple Insurance Policies

Rental car accidents often involve a messy web of insurance policies: your personal auto insurance, the credit card company, the rental agency’s fleet insurance, and the at-fault driver’s policy. If insurers are pointing fingers at each other and denying liability, an attorney can cut through the red tape and prevent you from being unfairly billed for damages.

Protecting Your Rights if You Suffer Injuries

Property damage is one thing, but physical injuries are another. If you or your passengers were injured in a rental car crash, you should consult a personal injury lawyer immediately. Insurance companies will try to minimize your payout for medical bills, lost wages, and pain and suffering. Legal representation ensures your rights are protected while you focus on recovery.