Table of contents

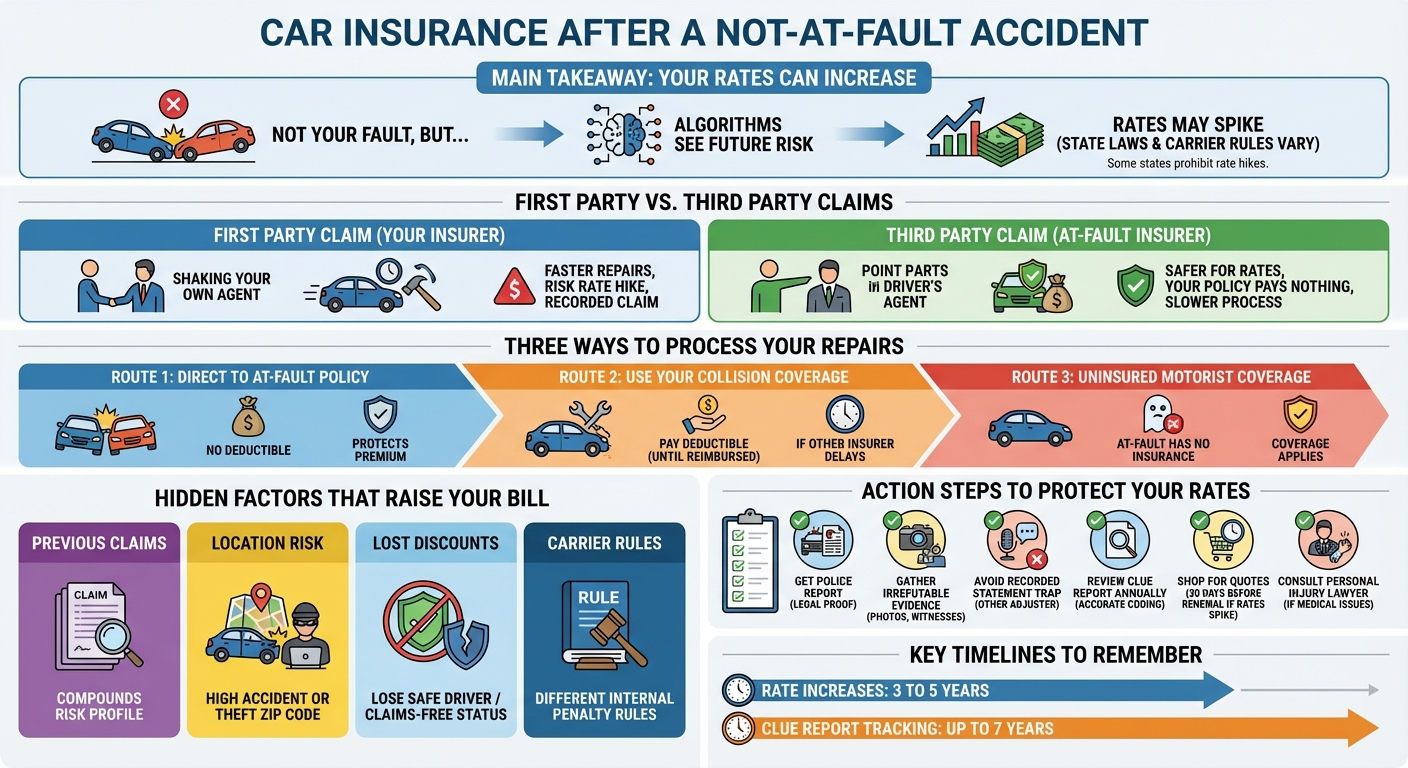

If someone hits your car, your insurance rates can still go up, even if you are not at fault. Insurers use risk algorithms that may flag you as a higher risk simply for being in an accident. However, rate increases depend heavily on your state laws, your specific carrier, and whether you file a claim.

If Someone Hits Your Car, Does Your Insurance Go Up?

The short answer is: Yes, it can, but it depends heavily on your state laws and your specific insurance carrier. It feels incredibly unfair to see your premiums spike when another driver crashes into you, but the reality of the insurance industry is driven by data, not fairness.

Why Insurance Companies Penalize Not-At-Fault Drivers

Insurance companies rely on complex risk algorithms to determine your monthly premium. To an insurer, statistics show that a driver who has been in one accident—regardless of fault—is statistically more likely to be involved in another accident in the future. Because you are now categorized in a higher risk bracket, the algorithm may automatically trigger a rate increase at your next policy renewal.

Will it affect my insurance if someone hits me?

Yes, it might affect your insurance if someone hits you. Even if you are 100% not at fault, filing a claim through your own policy or being involved in an accident can flag you as a higher risk in your insurer’s algorithm, potentially leading to a rate increase at renewal.

Will my insurance go up if it was someone else’s fault?

Your insurance may go up if it was someone else’s fault, particularly if you file a claim under your own collision or uninsured motorist coverage. However, if you file a third-party claim directly with the at-fault driver’s insurance company, your rates are much less likely to increase.

First-Party Claims vs. Third-Party Claims: What You Need to Know

- First-Party Claim: You file the claim with your own insurance company. Your insurer pays for your repairs upfront (minus your deductible) and then attempts to get reimbursed by the at-fault driver’s insurer. This is faster but puts a claim directly on your record, increasing the odds of a rate hike.

- Third-Party Claim: You file the claim directly with the at-fault driver’s insurance company. Because your insurer is not paying out any money, your rates are generally safer.

State Laws That Protect Drivers from Not-At-Fault Rate Hikes

Fortunately, where you live matters. Several states have consumer protection laws that prohibit insurance companies from raising your premiums after a not-at-fault accident. For example, in Texas, state regulations generally forbid insurers from increasing your rates for an accident you did not cause, provided you have the police report and evidence to prove the other driver was entirely at fault.

How does insurance work if it’s not your fault?

If an accident is not your fault, insurance works by holding the at-fault driver’s liability coverage responsible for your property damage and medical bills. You can either file a claim directly with their insurer, or use your own coverage and let your insurer recover the costs later through a process called subrogation.

Step 1: Filing Against the At-Fault Driver’s Liability Policy

This is the ideal route. You contact the other driver’s insurance company, provide the police report and evidence, and they cover your vehicle repairs and medical expenses. You pay no deductible, and your own insurance rates remain untouched.

Step 2: Using Your Own Collision Coverage (and the Subrogation Process)

If the other driver’s insurance is dragging their feet, you can use your own collision coverage to fix your car immediately. You will have to pay your deductible. Your insurance company will then enter subrogation—a legal process where they demand reimbursement from the at-fault driver’s insurer. If successful, your insurer will refund your deductible.

Step 3: Dealing with Uninsured or Underinsured Drivers

If the person who hit you has no insurance, you will need to rely on your Uninsured Motorist (UM) coverage. While this is a first-party claim, many states restrict insurers from severely penalizing drivers for using the UM coverage they pay for.

How long does your car insurance go up if someone hits you?

If your car insurance goes up after someone hits you, the rate increase typically lasts for three to five years. Most insurance companies use a surcharge schedule that keeps the accident on your premium record for 36 to 60 months before your rates gradually return to normal.

How to Check Your CLUE Report

Insurance companies track your claims history using the Comprehensive Loss Underwriting Exchange (CLUE) report. This database records every claim associated with your vehicle and name for up to seven years. You are entitled to one free copy of your CLUE report every 12 months, which you can use to verify that a not-at-fault accident is coded correctly.

When to Shop Around for a New Insurance Carrier

If your current insurer hikes your rates significantly after an accident you didn’t cause, do not just accept it. Different insurers weigh not-at-fault accidents differently. Shopping around for quotes 30 days before your renewal date can help you find a carrier with a more forgiving algorithm.

4 Hidden Factors That Influence Your Premium After a Crash

Beyond the accident itself, insurers look at several hidden variables when calculating your new premium:

- Your Previous Claims History (The ‘Frequent Filer’ Penalty): If you have filed multiple claims in the past three years—even minor ones—another accident will compound your risk profile.

- Your Zip Code and Local Accident Density: If the accident occurred in an area that has recently seen a spike in crashes or auto thefts, your base rate may increase simply due to regional risk adjustments.

- Loss of a ‘Claims-Free’ Discount: Even if your base rate doesn’t go up, you might lose a lucrative “claims-free” or “safe driver” discount, resulting in a higher overall bill.

- The Carrier’s Internal Surcharge Policies: Every company has proprietary rules. Carrier A might ignore a not-at-fault crash entirely, while Carrier B might impose a 10% surcharge.

How to Protect Your Rates and Your Rights After a Not-At-Fault Accident

Protecting your wallet starts the moment the crash happens. Take these steps to ensure you aren’t unfairly penalized:

- Always get a police report: A police report is the ultimate tool to prove fault definitively. Without it, the other driver’s insurance company may try to pin partial blame on you.

- Gather irrefutable evidence at the scene: Take extensive photos of the vehicles, the road conditions, and gather witness contact information. Learn more about documenting your Texas accident scene to build a bulletproof case.

- Beware of the recorded statement trap: The at-fault driver’s insurance adjuster will call you, acting friendly, and ask for a recorded statement. They are looking for ways to shift the blame onto you. Read up on the recorded statement trap before you speak to them.

- Consult a personal injury lawyer: If you suffered injuries, a lawyer can handle the insurance companies for you, ensuring fault is placed exactly where it belongs so your financial future—and your insurance rates—are protected.