Table of contents

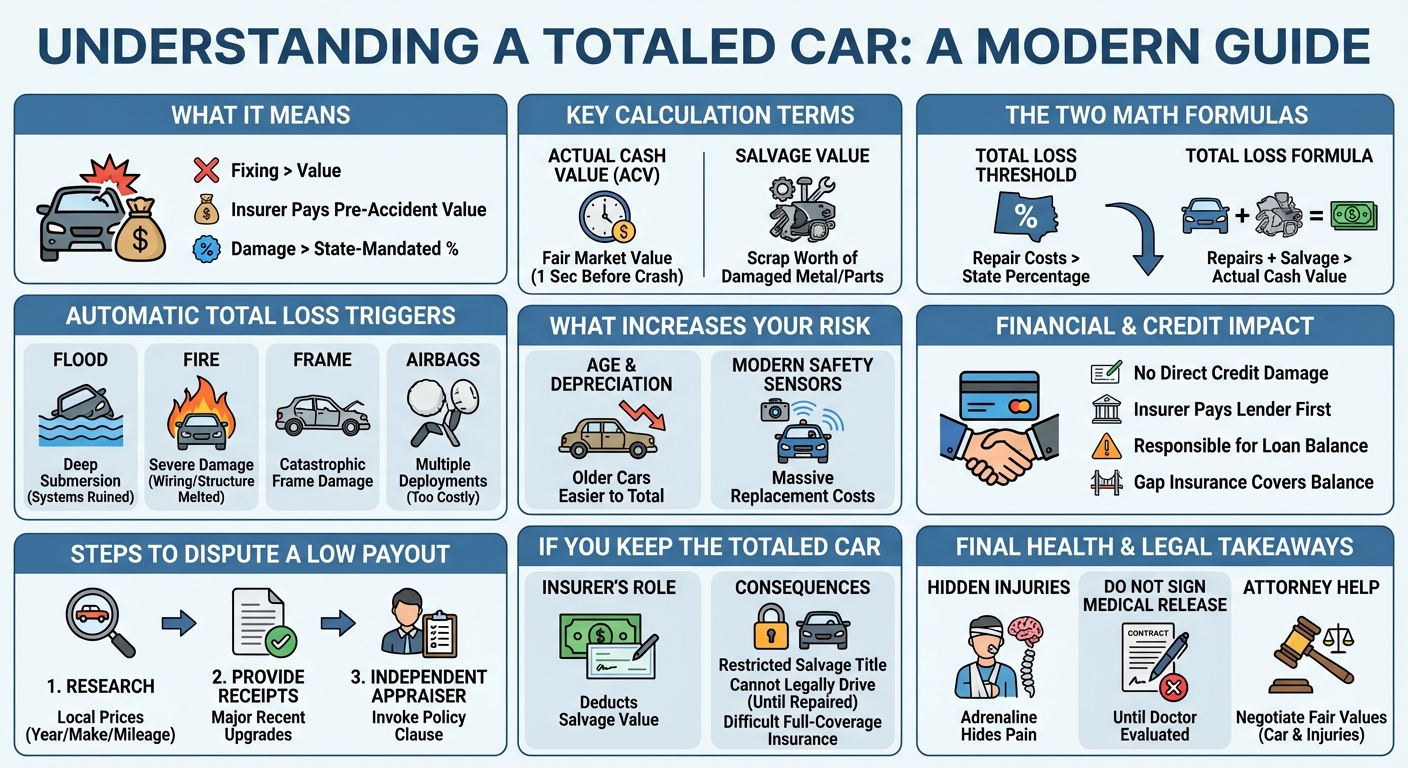

A car is considered totaled when the cost to repair it exceeds its Actual Cash Value (ACV) or a specific state-mandated percentage of that value. Insurance companies calculate this using either a Total Loss Threshold, typically between 70% and 100%, or a Total Loss Formula that factors in the vehicle’s salvage value.

What Does It Mean When a Car is Totaled?

Hearing that your vehicle is a total loss can be overwhelming. In the insurance world, a totaled car simply means that the vehicle is no longer economically viable to repair. Rather than paying a body shop to fix the extensive damage, the insurance company decides it makes more financial sense to pay you the pre-accident value of the vehicle.

What does it take for my car to be totaled?

For your car to be totaled, the estimated cost of repairs plus the salvage value must exceed the vehicle’s actual cash value (ACV). Alternatively, repairs must simply cross your state’s specific total loss threshold, which typically ranges from 70% to 100% of the car’s pre-accident market value.

How Insurance Companies Calculate a Total Loss

Insurance adjusters do not guess when declaring a total loss. They use strict mathematical formulas and state regulations to determine if a car should be repaired or sent to the salvage yard.

Actual Cash Value (ACV) vs. Repair Costs

The foundation of a total loss calculation is the Actual Cash Value (ACV). This is not what you paid for the car, nor is it the cost to buy a brand-new replacement. ACV is the fair market value of your specific vehicle exactly one second before the crash. Adjusters calculate ACV by looking at your car’s age, mileage, condition, trim level, and local sales data for similar vehicles. They then compare this ACV against the body shop’s repair estimate.

Understanding Salvage Value

Even a completely wrecked car has some worth. The salvage value is the amount a scrapyard or parts dealer will pay for the damaged vehicle’s remaining metal and usable parts. Insurance companies factor this into their math to determine their net loss on the claim.

State Laws: Total Loss Threshold (TLT) vs. Total Loss Formula (TLF)

State laws dictate exactly how insurance companies must calculate a total loss. States generally use one of two systems:

| Calculation Method | How It Works | Where It Is Used |

|---|---|---|

| Total Loss Threshold (TLT) | The state sets a specific percentage (e.g., 75%). If repair costs exceed 75% of the ACV, the car is totaled. | Many US states (e.g., Texas uses 100%, New York uses 75%). |

| Total Loss Formula (TLF) | Cost of Repairs + Salvage Value > Actual Cash Value. If true, the car is totaled. | States without a mandated threshold percentage. |

What makes a car automatically totaled?

A car is automatically totaled when it sustains catastrophic damage that makes it impossible or illegal to repair safely. This typically includes severe fire damage, deep floodwater submersion, or extreme structural compromises where the repair costs definitively exceed the vehicle’s actual cash value before an estimate is even finished.

Fire Damage and Flooding

Water and fire destroy the core components of a vehicle. Floodwater ruins complex electrical systems, engine internals, and safety sensors, leading to a near-guaranteed total loss. Similarly, fire compromises the structural integrity of the metal and melts wiring harnesses, making safe repair impossible.

Severe Structural and Frame Damage

While minor frame damage can sometimes be pulled and straightened, severe structural crumpling compromises the safety cage of the vehicle. If the frame cannot be restored to factory safety specifications, the insurer will automatically total the car to avoid liability in future accidents.

Airbag Deployment Costs

Replacing deployed airbags is incredibly expensive. A single airbag replacement can cost thousands of dollars because it requires replacing the bag, the sensors, the steering wheel cover, and often the dashboard. If multiple airbags deploy in an older vehicle, the cost of the airbags alone is usually enough to total the car.

How likely will my car be totaled?

The likelihood of your car being totaled depends heavily on its age, pre-crash value, and the severity of the damage. Older vehicles depreciate, making them much more likely to be totaled from minor accidents, whereas newer cars usually require significant structural damage or airbag deployment to reach the total loss threshold.

The Impact of Vehicle Age and Depreciation

Because cars depreciate rapidly, a 10-year-old sedan has a much lower ACV than a brand-new SUV. A minor fender bender that costs $3,000 to fix might be a simple repair on a new car, but it could easily exceed the total loss threshold of an older, heavily depreciated vehicle.

Modern Car Sensors and Expensive Calibrations

Modern vehicles are packed with advanced driver-assistance systems (ADAS), cameras, and radar sensors located in the bumpers and windshields. A seemingly minor collision can destroy these sensitive components. The cost to replace and recalibrate these sensors is skyrocketing, leading to higher repair estimates and an increased likelihood of a total loss.

Does totaling a car affect your credit?

Totaling a car does not directly affect your credit score. However, if you owe more on your auto loan than the insurance payout and fail to pay the remaining balance, missed payments will negatively impact your credit. Using gap insurance can protect your credit by covering this remaining difference.

Auto Loans, Gap Insurance, and Credit Scores

When your car is totaled, the insurance company pays the ACV directly to your lender first. If the ACV covers your loan, your loan is closed. If you have Gap Insurance, it steps in to pay any remaining balance. As long as the loan is paid off, your credit score remains perfectly safe.

What Happens if You Owe More Than the Car is Worth?

Being underwater on a car loan is a stressful position after an accident. If the insurance payout is $10,000 but you owe $13,000, you are personally responsible for the remaining $3,000. If you stop making payments on that $3,000, your lender will report the delinquency to credit bureaus, which will severely damage your credit score.

What to Do If You Disagree with the Insurance Company

Insurance companies want to minimize their payouts. Their initial ACV offer is often a lowball estimate. You do not have to accept their first offer if you believe your car is worth more.

How to Dispute the Actual Cash Value

Do your own research. Look up the retail value of your exact make, model, year, and mileage on sites like Kelley Blue Book or Edmunds. Search local dealership listings for identical cars in your area. If the insurer’s comparable vehicles are in worse condition than yours, point out the discrepancies.

Providing Proof of Upgrades and Maintenance

Standard maintenance (like oil changes) will not increase your car’s value, but major recent investments might. If you recently installed a brand-new transmission, custom wheels, or a premium sound system, provide the receipts to the adjuster. They may adjust the ACV upward.

Invoking the Appraisal Clause

If negotiations stall, check your insurance policy for an appraisal clause. This allows you to hire an independent appraiser to value your vehicle. The insurance company will also hire one. If the two appraisers cannot agree, a neutral third-party umpire makes the final, binding decision.

Can You Keep a Totaled Car?

In most states, you have the right to keep your totaled vehicle, but it comes with significant financial and legal strings attached.

Owner Retention Payout Reductions

If you decide to keep the car, the insurance company will deduct the vehicle’s salvage value from your payout. For example, if your car’s ACV is $10,000 and its salvage value is $2,000, the insurer will hand you a check for $8,000 and let you keep the damaged vehicle.

Rebuilt Titles and Future Insurance Challenges

Keeping a totaled car means your state DMV will issue a salvage title. You cannot legally drive a car with a salvage title. You must repair it out of pocket, pass a rigorous state safety inspection, and apply for a rebuilt title. Even then, many insurance companies refuse to offer comprehensive or collision coverage on rebuilt vehicles.

Protecting Your Rights After a Severe Accident

Dealing with property damage is only half the battle. A collision violent enough to total a modern vehicle involves massive transfer of kinetic energy, which takes a toll on the human body.

Why Severe Property Damage Often Equals Hidden Injuries

If the steel frame of your car was bent and airbags were deployed, your spine, neck, and joints absorbed a massive shock. Adrenaline often masks the pain of whiplash, soft tissue injuries, or herniated discs for days or even weeks. Never sign a medical release or accept a bodily injury settlement from the insurance company until you have been fully evaluated by a medical professional.

How a Car Accident Lawyer Can Help Maximize Your Claim

Insurance adjusters are trained to close claims quickly and cheaply. While you are fighting over the fair market value of your totaled car, they may try to pressure you into a lowball injury settlement. An experienced personal injury attorney can handle the aggressive negotiations, ensure your property damage is valued fairly, and fight to get you the maximum compensation for your physical injuries and lost wages.