Table of contents

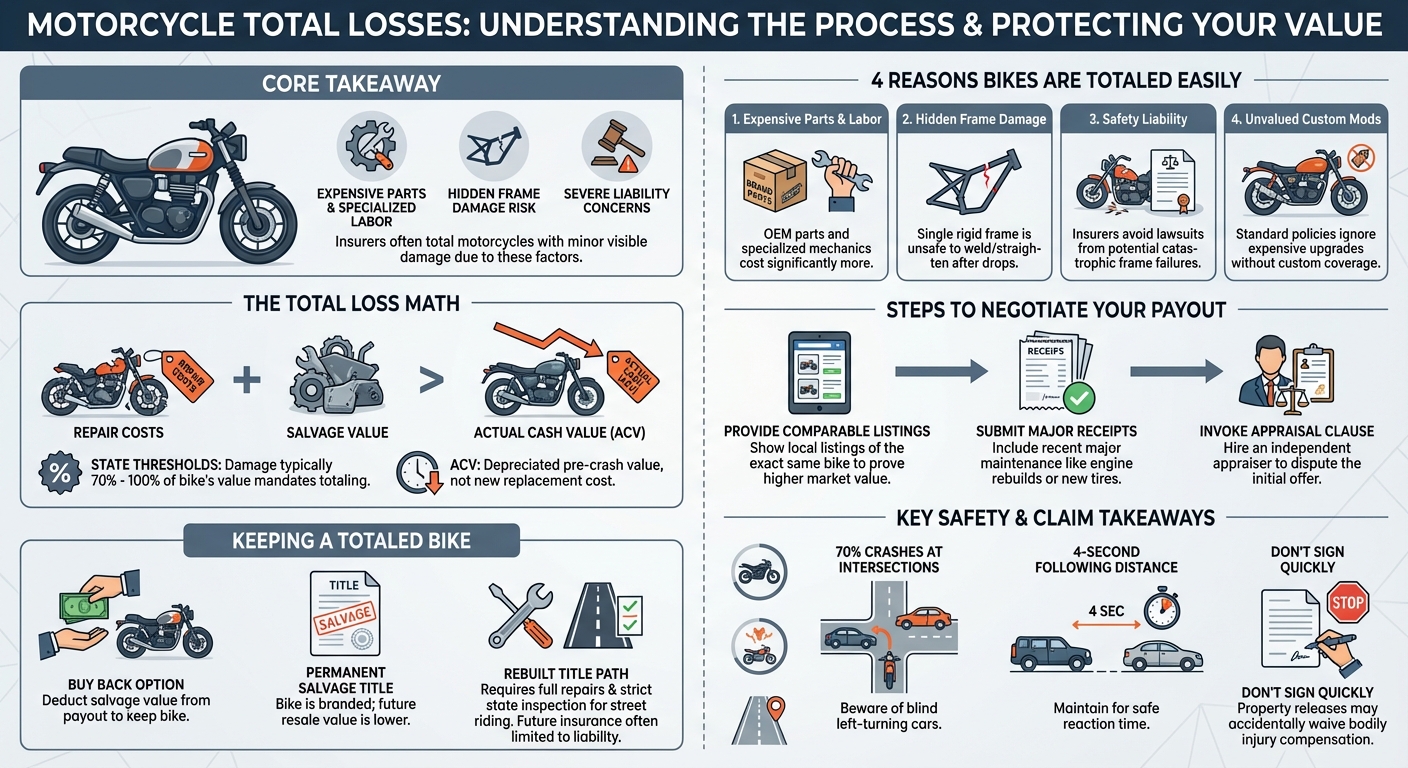

Insurance companies total motorcycles with little visible damage because the cost of Original Equipment Manufacturer (OEM) parts and specialized labor is exceptionally high. Additionally, even minor drops can cause hidden frame damage. Insurers prefer declaring a total loss rather than risking liability for unsafe structural repairs.

It is one of the most frustrating experiences for a rider: you drop your bike, suffer what looks like minor cosmetic scratches to the fairings and exhaust, and the insurance adjuster declares it a total loss. To the naked eye, the bike looks perfectly fixable. To the insurance company, it is a financial liability.

Understanding how insurance adjusters evaluate motorcycle damage can help you negotiate a better payout or decide if buying back your salvage-title bike is worth the risk.

Why do motorcycles get totaled so easily?

Motorcycles get totaled easily because even minor drops can cause hidden structural damage to the frame, which is expensive or impossible to safely repair. Additionally, the high cost of Original Equipment Manufacturer (OEM) parts and specialized labor quickly pushes the repair estimate past the bike’s actual cash value.

What makes a motorcycle considered totaled?

A motorcycle is considered totaled when the estimated cost to repair the damage, plus its salvage value, exceeds the insurance company’s total loss threshold. Depending on state regulations, this threshold typically ranges between 70% and 100% of the motorcycle’s actual cash value prior to the accident.

The Total Loss Formula (TLF) and State Thresholds

Insurance companies use specific formulas to determine if a vehicle is worth fixing. Many states mandate a Total Loss Threshold (TLT). For example, if a state has an 80% threshold, a bike worth $10,000 will be totaled if repairs exceed $8,000.

In states without a strict percentage threshold, insurers use the Total Loss Formula (TLF): Cost of Repairs + Salvage Value > Actual Cash Value. If the math shows the insurer loses less money by cutting you a check and selling the wrecked bike at a salvage auction, they will total it.

Understanding Actual Cash Value (ACV) vs. Replacement Cost

A common point of friction is the difference between Actual Cash Value and Replacement Cost.

- Actual Cash Value (ACV): What your bike was worth the second before the crash, factoring in age, mileage, and depreciation.

- Replacement Cost: What it would cost to buy a brand-new version of your motorcycle today.

Standard auto and motorcycle policies only pay out the ACV. Because motorcycles depreciate quickly, the ACV is often much lower than riders expect, making the total loss threshold easier to cross.

4 Reasons Insurers Total Bikes With Minimal Visible Damage

1. The High Cost of OEM Parts and Specialized Labor

Motorcycle parts are disproportionately expensive compared to car parts. A single scratched OEM fairing, a dented gas tank, or a scuffed exhaust pipe can cost thousands of dollars to replace. Furthermore, motorcycle repair requires specialized mechanics who charge higher hourly labor rates than standard auto body shops.

2. Hidden Structural and Frame Damage

Unlike cars, which have crumple zones and modular frames, motorcycles rely on a single, rigid frame for stability and safety. Even a low-speed tip-over can scratch, bend, or crack the frame. Most manufacturers strongly advise against welding or straightening a damaged motorcycle frame. If the frame is compromised, the entire frame must be replaced—a highly labor-intensive process that almost guarantees a total loss.

3. Liability and Post-Repair Safety Concerns

Insurance companies are risk-averse. If an insurer authorizes a repair on a structurally questionable motorcycle and the frame fails at 70 mph, the insurer and the repair shop could face a massive liability lawsuit. It is financially safer for the insurance company to total the bike rather than risk a catastrophic post-repair failure.

4. Custom Upgrades and Modifications Aren’t Fully Valued

Many riders invest heavily in aftermarket exhausts, custom paint, upgraded suspensions, and chrome accessories. Unfortunately, standard insurance policies do not add the dollar-for-dollar value of these upgrades to your bike’s ACV. Unless you purchased specific “custom parts and equipment” (CPE) coverage, the insurer values your bike based on its stock configuration, meaning your expensive upgrades won’t protect the bike from being totaled.

What to Do When Your Insurance Company Totals Your Motorcycle

How to Dispute and Negotiate the Actual Cash Value

If you believe the insurance company is lowballing your motorcycle’s ACV, you do not have to accept their first offer. You can fight back by:

- Providing comparables (comps): Find listings for the exact same make, model, year, and mileage in your local area to prove the market value is higher.

- Submitting maintenance records: Show receipts for recent major work, such as a new engine rebuild or brand-new tires, which can incrementally increase the ACV.

- Invoking the appraisal clause: Most policies allow you to hire an independent appraiser to evaluate the bike if you and the insurer cannot agree on the value.

Buying Back Your Bike: Understanding Salvage Titles

If you want to keep your totaled bike—perhaps to turn it into a track bike or part it out—you can usually “buy it back” from the insurance company. The insurer will deduct the bike’s salvage value from your payout and let you keep it.

However, the bike will be issued a salvage title. To ride it legally on the street again, you must repair it and pass a rigorous state inspection to get a rebuilt title. Even then, most insurance companies will only offer liability coverage on a rebuilt title, refusing to provide collision or comprehensive coverage.

Motorcycle Safety and Accident Facts You Should Know

Where do 70% of motorcycle accidents occur?

Approximately 70% of motorcycle accidents occur at intersections. These dangerous collisions most frequently happen when a passenger vehicle driver fails to see the approaching motorcyclist and makes a left turn directly into the rider’s path, leaving the biker with little to no time to avoid the crash.

What is the 4 second rule on a motorcycle?

The 4 second rule on a motorcycle is a crucial safe following distance guideline. It recommends that riders stay at least four seconds behind the vehicle directly in front of them. This buffer provides adequate time to react, brake safely, or swerve if traffic suddenly stops.

Don’t Let a Quick Property Damage Payout Ruin Your Injury Claim

Insurance adjusters often rush to settle motorcycle property damage claims. They know that if they can get you to sign a release for a quick check, they might also be tricking you into releasing them from liability for your bodily injuries.

Never sign a property damage release without reading the fine print carefully. If you suffered any injuries in the crash—even minor road rash or a concussion—consulting with a personal injury attorney before dealing with the insurance company can protect your right to full compensation for both your bike and your health.