Table of contents

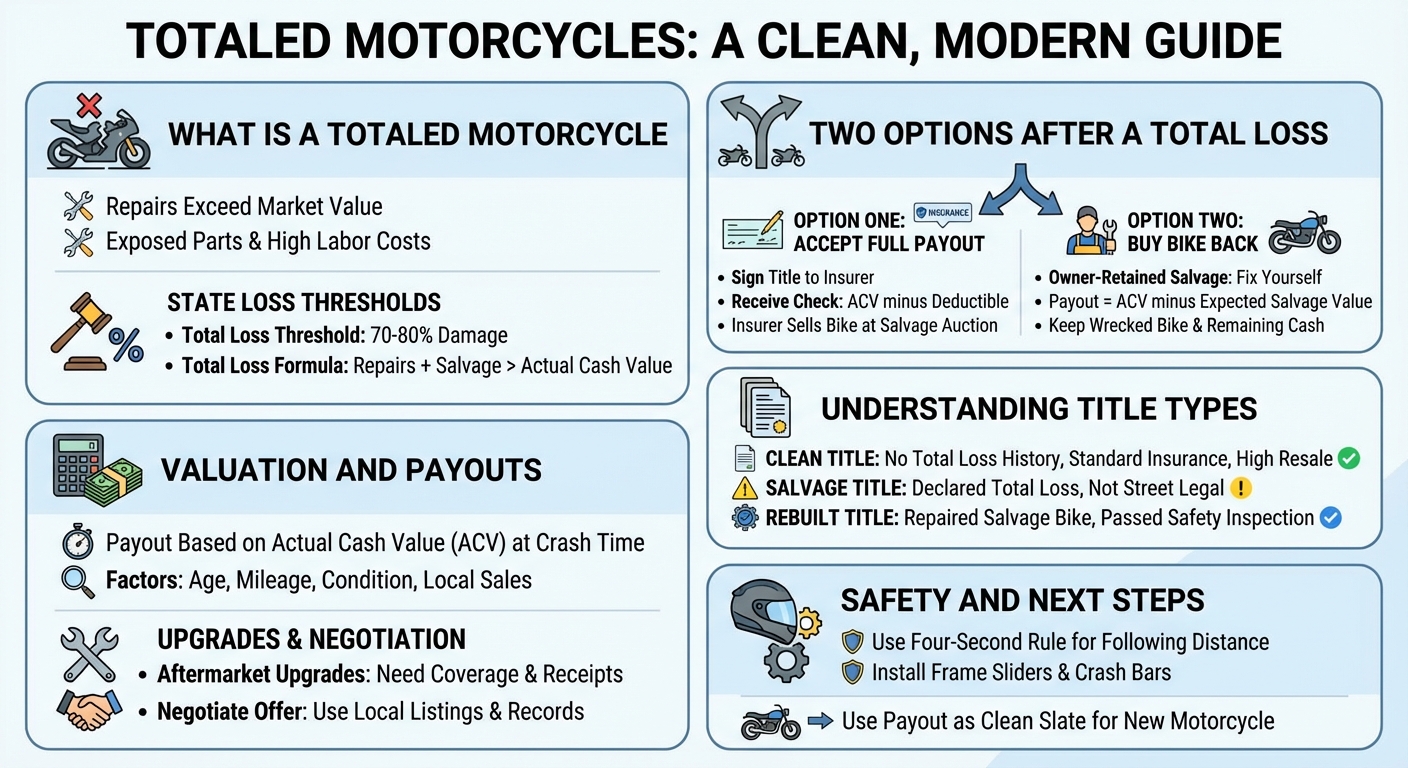

A motorcycle is considered totaled when the cost to repair the damage exceeds its Actual Cash Value (ACV) or a state-mandated total loss threshold. In these cases, the insurance company will declare the bike a total loss and pay you its pre-accident market value instead of paying for repairs.

Understanding Totaled Motorcycles: Insurance, Payouts, and Salvage Titles

Having your motorcycle involved in an accident is stressful enough, but hearing your insurance company declare it a “total loss” can add a layer of financial confusion. Whether you are trying to understand your insurance payout, considering buying your wrecked bike back, or looking to purchase a repairable salvage motorcycle from an auction, knowing how totaled motorcycles are valued and processed is essential.

What Exactly Is a Totaled Motorcycle?

A motorcycle is considered totaled when the cost to repair the damage exceeds its pre-accident market value, or a specific percentage of that value dictated by state law. Insurance companies are businesses; if fixing the bike costs more than replacing it, they will opt to total it.

The Total Loss Formula (TLF) and State Thresholds

Insurance companies typically use one of two methods to declare a total loss:

- Total Loss Threshold (TLT): Many states mandate a specific threshold, usually between 70% and 80%. If the repair costs hit this percentage of the bike’s value, it must be totaled.

- Total Loss Formula (TLF): In states without a strict threshold, insurers use the TLF: Cost of Repairs + Salvage Value > Actual Cash Value. If the math checks out, the bike is totaled.

Actual Cash Value (ACV) vs. Repair Costs

Your payout is based on the Actual Cash Value (ACV), not what you originally paid for the bike or what it costs to buy a brand-new replacement. ACV is the fair market value of your motorcycle exactly one second before the crash, factoring in depreciation, mileage, and wear and tear.

Why do motorcycles get totaled so easily?

Motorcycles lack a protective outer frame, meaning even low-speed drops can severely damage expensive components like the chassis, engine cases, or forks. Because original replacement parts and specialized labor rates are notoriously high, repair costs quickly surpass the bike’s actual cash value, resulting in a total loss.

The Insurance Process: Payouts and Valuations

How do insurance companies value a totaled motorcycle?

Insurance companies value a totaled motorcycle by determining its Actual Cash Value (ACV) immediately before the accident. They use proprietary valuation software, recent sales of comparable bikes in your local area, dealership quotes, and standard depreciation metrics based on the motorcycle’s age, mileage, and pre-crash condition.

Factoring in Aftermarket Modifications and Upgrades

Motorcyclists love to customize, but standard insurance policies rarely cover aftermarket exhaust systems, custom paint, or upgraded suspension automatically. To get compensated for these, you usually need specific accessory coverage. Always keep your receipts; if your bike is totaled, presenting proof of recent upgrades can sometimes bump up your ACV.

Negotiating Your Total Loss Settlement

You do not have to accept the first number the insurance adjuster gives you. If you believe your bike is worth more, you can negotiate by providing:

- Listings of similar motorcycles for sale in your zip code.

- Maintenance records proving exceptional condition.

- Receipts for recent major mechanical work (like a fresh engine rebuild).

What Happens After Your Motorcycle Is Totaled?

Option 1: Accepting the Full Insurance Payout

This is the most common route. You sign the title over to the insurance company, they cut you a check for the ACV (minus your deductible), and they take the wrecked bike to a salvage auction like Copart or CrashedToys.

Option 2: Owner-Retained Salvage (Buying Your Bike Back)

If the damage is mostly cosmetic and you want to fix it yourself, you can choose owner-retained salvage. The insurance company will deduct the “salvage value” (what they would have made selling it at auction) from your payout. You keep the bike and the remaining cash.

Understanding Salvage and Rebuilt Titles

Keeping a totaled bike changes its legal status. Here is a quick breakdown of title types:

| Title Type | Definition | Insurability | Resale Value |

|---|---|---|---|

| Clean | No major accidents or total loss history. | Standard | High |

| Salvage | Declared a total loss by an insurance company. Not street legal. | Very Difficult | Low |

| Rebuilt | A salvage bike that has been repaired and passed a state safety inspection. | Liability Only (Usually) | Moderate |

Should You Buy a Totaled or Salvage Motorcycle?

Pros and Cons of Buying Salvage Bikes

Buying a salvage motorcycle can be a great deal, but it comes with risks.

- Pros: Significantly lower purchase price; great source for spare parts; ideal for building a dedicated track-day bike where titles do not matter.

- Cons: Hidden structural damage (like a bent frame) is common; difficult to finance through a bank; comprehensive insurance is rarely available.

Where to Find Repairable Motorcycles (Auctions & Dealers)

If you are mechanically inclined, you can find repairable salvage motorcycles at major auction platforms like CrashedToys, Copart, and IAAI. Many local salvage motorcycle dealers also buy these bikes, do the baseline repairs, and sell them to the public.

Motorcycle Safety and Preventing Total Loss Accidents

What is the 4 second rule on a motorcycle?

The 4-second rule is a crucial following distance guideline for motorcyclists. It advises riders to maintain at least four seconds of space between their motorcycle and the vehicle ahead. This buffer provides adequate time to safely react, brake, or swerve if the leading vehicle stops suddenly.

Defensive Riding Strategies to Protect Your Investment

Beyond following distances, protecting your bike from a total loss involves hyper-awareness. Always assume drivers cannot see you, avoid lingering in blind spots, and invest in frame sliders or crash bars. These simple bolt-on accessories can absorb the impact of a drop, saving your engine cases and fairings from total-loss-level damage.

Replacing Your Ride: Moving On After a Total Loss

Which bike is most liked by girls?

While preferences vary widely, female riders often favor motorcycles with lower seat heights, manageable weight, and smooth power delivery. Popular choices include the Honda Rebel 500, Kawasaki Ninja 400, and Harley-Davidson Sportster, as they offer an excellent balance of comfort, style, and confidence-inspiring ergonomics.

Choosing the Right Replacement Motorcycle for Your Riding Style

A total loss is a frustrating setback, but it is also a clean slate. When using your insurance payout to buy a new motorcycle, consider how your riding habits have evolved. If your totaled sportbike was uncomfortable on long trips, this might be the perfect time to transition to an adventure bike or a cruiser.