Table of contents

An insurance company totals a car when the cost to repair the damage exceeds the vehicle’s actual cash value (ACV) or a state-mandated percentage. Insurers use either a Total Loss Threshold (typically 70% to 100% of the car’s value) or a Total Loss Formula to make this financial decision.

Understanding When and Why Insurance Companies Total a Car

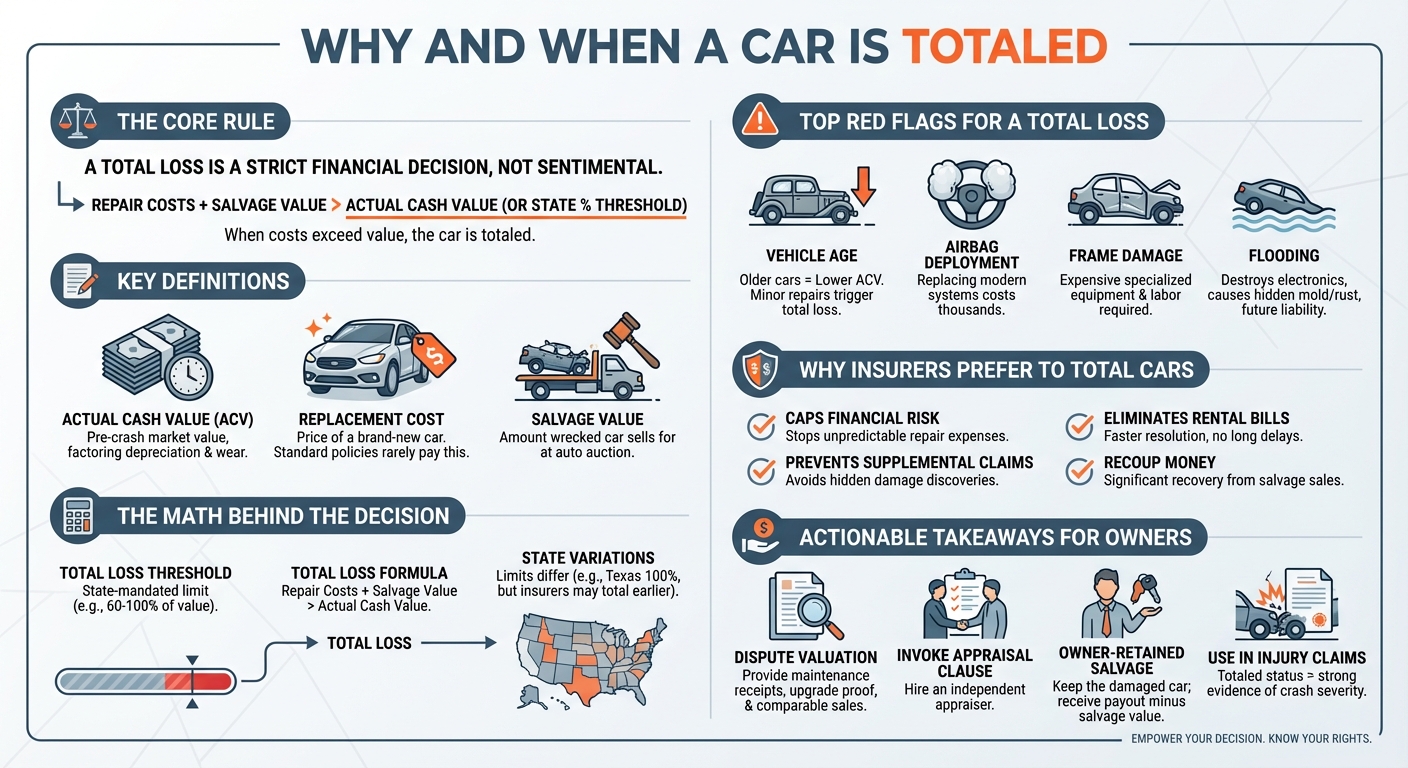

After a severe accident, waiting to hear if your vehicle is repairable can be stressful. Insurance companies do not make this decision based on sentiment; it is a strict financial calculation.

What makes a car automatically totaled?

A car is automatically totaled when the cost to repair it, plus its salvage value, exceeds its actual cash value (ACV), or when state law mandates it based on a specific Total Loss Threshold (TLT). Severe structural damage, flooding, or fire often trigger an automatic total loss.

Defining Actual Cash Value (ACV) vs. Replacement Cost

To understand total loss calculations, you must understand how insurers value your vehicle. Actual Cash Value (ACV) is the vehicle’s pre-crash market value, factoring in depreciation, mileage, and wear-and-tear. It is what your car would have sold for the second before the crash. Replacement Cost is the amount required to buy a brand-new version of your car. Standard auto policies only pay ACV, meaning you rarely get enough to buy a brand-new replacement.

The difference between repairable damage and a structural total loss

Cosmetic damage—like dented doors or shattered windows—is usually straightforward to fix. However, if the vehicle’s frame is bent or the structural integrity is compromised, the labor hours required to safely restore the car skyrocket. When structural repairs push the estimate near the vehicle’s ACV, the insurer will write it off rather than risk unsafe repairs.

The Math Behind the Decision: Thresholds and Formulas

Insurers use specific mathematical formulas and state regulations to determine when to pull the plug on repairs.

What percentage of car value to total?

The percentage of a car’s value required to total it depends on your state’s laws, typically ranging from 60% to 100%. Many states use a Total Loss Threshold (TLT) of around 70% to 80% of the vehicle’s actual cash value, while others rely on the Total Loss Formula.

Total Loss Threshold (TLT) explained (State-by-State variations)

Many states dictate exactly when an insurer must declare a vehicle a total loss. This is known as the Total Loss Threshold (TLT). For example, if a state has a 75% TLT, and your car’s ACV is $10,000, the insurance company must total the car if repair estimates reach $7,500.

How the Total Loss Formula (TLF) works (Cost of Repairs + Salvage Value > ACV)

In states without a strict TLT, insurers use the Total Loss Formula (TLF). The formula is simple: if the Cost of Repairs plus the Salvage Value (what the wrecked car can be sold for at auction) equals or exceeds the Actual Cash Value, the car is totaled. This formula protects the insurer’s bottom line.

Texas specific rules for total loss vehicles

Texas uses a 100% Total Loss Threshold. Under Texas law, a vehicle is legally considered a total loss only if the repair costs equal or exceed the actual cash value of the vehicle. However, insurance companies in Texas can still choose to total a vehicle earlier if it makes financial sense under their own internal Total Loss Formula.

The Insurance Company’s Hidden Incentives

You might wonder why an insurer would total a car that looks perfectly fixable. The answer lies in risk management and hidden revenue streams.

Why are insurance companies quick to total a car?

Insurance companies are quick to total a car because it limits their financial risk. By declaring a total loss, insurers avoid paying for hidden damages discovered during repairs, eliminate extended rental car costs, and can recoup a significant portion of their payout by selling the totaled vehicle at a salvage auction.

The lucrative role of salvage value and auto auctions

When an insurer totals your car, they take ownership of it. They then sell the wreckage to massive salvage auction companies like Copart or IAA. The parts and scrap metal hold significant value. If an insurer pays you $15,000 for your totaled car but sells the salvage for $5,000, their net loss is only $10,000.

Avoiding supplemental repair claims and extended rental car payouts

Modern vehicles are packed with sensors, cameras, and complex wiring. Initial repair estimates often balloon once a mechanic starts tearing the car apart (known as a supplemental claim). Furthermore, supply chain delays mean cars sit in shops for months, racking up massive rental car bills for the insurer. Totaling the car cuts off these unpredictable expenses immediately.

Assessing Your Vehicle’s Damage

Not all accidents result in a total loss, but certain factors drastically increase the odds.

How likely will my car be totaled?

Your car is highly likely to be totaled if it is an older model with high mileage, sustained significant frame damage, had multiple airbags deploy, or suffered flood or fire damage. Because older vehicles have a lower actual cash value, even minor cosmetic repairs can quickly exceed their threshold.

Red flags for a total loss: Airbag deployment, frame damage, and flooding

- Airbag Deployment: Replacing a modern airbag system can cost thousands of dollars. If multiple airbags deploy, the repair bill often instantly exceeds the car’s value.

- Frame Damage: Straightening a bent frame requires specialized equipment and massive labor costs.

- Flooding: Water destroys electrical systems and causes hidden mold and rust. Insurers almost always total flooded cars due to the liability of future electrical failures.

Older vehicles vs. newer vehicles: Why age matters in total loss claims

Depreciation is the enemy of keeping your car. A minor fender bender that costs $3,000 to fix is a routine repair on a brand-new $40,000 SUV. That exact same $3,000 damage on a ten-year-old sedan worth $3,500 will result in an immediate total loss.

What to Do If Your Car Is Declared a Total Loss

If the adjuster calls with bad news, you still have rights and options.

How to dispute the insurance company’s ACV valuation

Insurers often lowball the ACV by using generic market data. You can fight back by providing evidence of your car’s true worth. Gather recent maintenance receipts, proof of aftermarket upgrades, and listings of comparable vehicles (same year, make, model, and mileage) selling in your local area. You can also invoke the appraisal clause in your policy to hire an independent appraiser.

Can you keep a totaled car? (Understanding owner-retained salvage)

Yes, in most states, you can choose to keep a totaled car. This is called owner-retained salvage. The insurer will deduct the salvage value from your final payout, and you will be left with the damaged car and a salvage title. You are then responsible for repairing it and passing state inspections to make it street-legal again.

How a totaled vehicle impacts your personal injury claim

A totaled car is a powerful piece of evidence in a personal injury case. Insurance adjusters frequently try to downplay injuries by claiming an accident was just a minor impact. Photographs of a completely destroyed, totaled vehicle make it incredibly difficult for them to deny the severity of the crash. For more information on protecting your rights after a severe crash, read our guide on The Truth About Dealing with Insurance Companies After a Houston Car Accident.