Table of contents

After your Houston car accident, one of the first things the insurance company will push to settle is your property damage claim. They’ll send an adjuster quickly, assess your vehicle, cut a check, and close that part of your file.

It seems efficient. It feels like progress. You’re getting some money, your car is getting fixed, and the process is moving forward.

But that fast settlement might be setting a trap for your injury claim—one you won’t fully understand until it’s too late.

The Hidden Connection Between Property Damage and Injury Claims

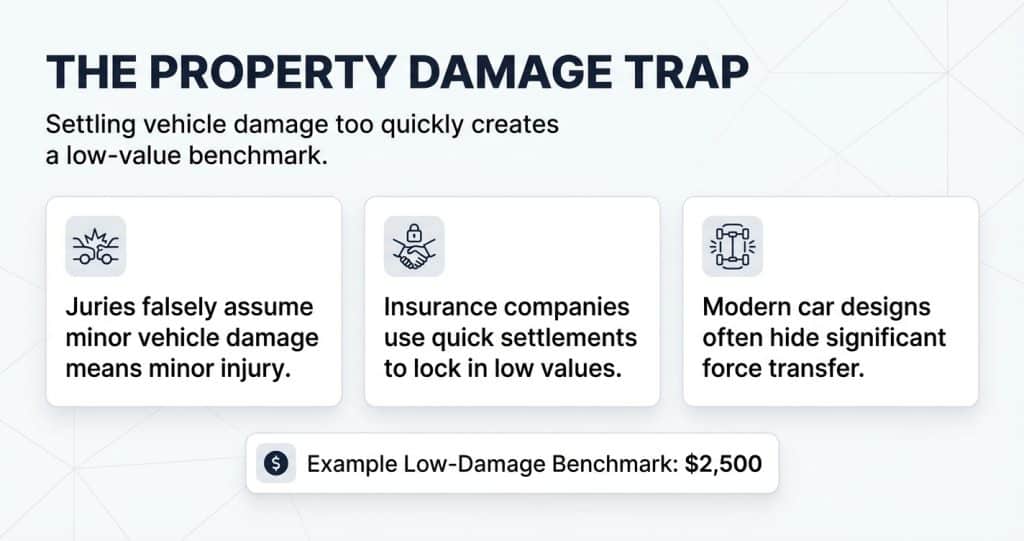

Here’s what insurance companies understand that most accident victims don’t: juries believe that serious injuries require serious vehicle damage.

It’s not always true—I’ve seen devastating injuries from low-speed accidents and people walk away from horrific crashes—but it’s a deeply held assumption that the insurance industry exploits ruthlessly.

By settling your property damage claim quickly and cheaply, the adjuster accomplishes two things:

- they save money on the vehicle claim itself. They have incentive to lowball the property damage estimate regardless of what happens with your injury claim.

- and more importantly, they create a number they can use against your injury claim forever. “Look at the property damage estimate,” they’ll argue. “Barely $2,500 in damage. How could she possibly have been seriously injured?”

That property damage number will follow you through negotiations, through mediation, through trial if it comes to that. It will appear in their settlement offers, their motion papers, their closing arguments. And once it’s locked in, there’s nothing you can do about it.

Why Property Damage and Injuries Don’t Correlate

The insurance industry wants you to believe that minor vehicle damage means minor injuries. They fund studies, train experts, and make arguments suggesting that real injuries can’t occur in low-speed collisions.

But the physics don’t actually support this correlation.

The damage to your vehicle depends on many factors: the design of the car, the materials used, how the vehicles aligned at impact, what crumple zones absorbed versus transferred force. Modern cars are specifically designed to sustain less visible damage in low-speed collisions—but that doesn’t mean the forces weren’t transferred to the occupants.

Meanwhile, the injuries you sustain depend on completely different factors: your position at impact, whether you saw it coming and braced yourself, your age and physical condition, any pre-existing vulnerabilities, the specific vectors of force through the cabin.

I’ve represented clients who were seriously injured in accidents that barely dented their bumpers. The person who was turned checking their blind spot when rear-ended. The elderly passenger with osteoporosis. The person with a pre-existing spinal condition that was dramatically aggravated. The woman whose seat belt failure caused injuries that wouldn’t have occurred in a higher-speed crash with a functioning belt.

Conversely, I’ve seen people walk away from catastrophic-looking accidents. A vehicle that rolls multiple times looks terrifying, but if the occupant was properly restrained and the safety systems worked, they might have only minor injuries.

The correlation between vehicle damage and injury severity is far weaker than the insurance industry wants you to believe.

The One-Adjuster Strategy

Here’s another trap to be aware of: many insurance companies now have the same adjuster handle both your property damage claim and your injury claim.

This creates a built-in conflict of interest that works against you.

That adjuster has every incentive to lowball your property damage estimate. The lower that number, the easier it is to argue your injuries must be minor. They’re essentially building ammunition against your injury claim while appearing to help you settle your car damage.

Even worse, the property damage interaction gives them a chance to evaluate you personally before your injury claim is seriously in play. They’re assessing your sophistication, your determination, your likelihood of hiring an attorney. They’re making notes about what kind of claimant you are. All of this happens under the guise of a routine property damage settlement.

Specific Tricks to Watch For

Insurance companies use several tactics to keep property damage valuations low:

- Incomplete appraisals. The adjuster inspects visible damage but doesn’t look for hidden damage to the frame, suspension, or alignment. After you settle, you discover additional problems that weren’t included.

- Unrealistic repair costs. They use parts prices and labor rates that don’t reflect what shops in your area actually charge. When you take the car for repairs, the body shop tells you it will cost more.

- Aftermarket parts valuations. They propose replacing your damaged OEM parts with cheaper aftermarket alternatives, reducing the repair estimate.

- Total loss lowballs. If your car is totaled, they offer less than fair market value, citing comparable sales that aren’t really comparable or using valuation methods that disadvantage you.

- Ignoring diminished value. After a significant accident, your car is worth less even after repairs—because it’s no longer “factory original” and has an accident on its record. Many adjusters refuse to address this real financial loss.

- Misleading photos. The adjuster takes photos that make the damage look minimal. These photos will show up later when they’re arguing you couldn’t have been seriously hurt.

What You Can Do

Don’t rush to settle property damage. I know you want your car fixed or replaced. I know you need transportation. But understand the implications before you sign anything.

Get your own documentation. Take extensive photos of your vehicle from every angle, including close-ups of all damage. Document any hidden damage discovered during repairs. Keep all repair estimates and invoices.

Understand what you’re signing. A property damage release typically only releases the property damage claim, not your injury claim. But make sure that’s actually what the document says before you sign it.

Consider waiting until your injury claim is clearer. If your injuries are significant, you may want to keep your property damage claim open while your injury situation develops. This prevents the early low number from being locked in.

Challenge low estimates. Get your own repair estimate from a reputable body shop. If there’s a significant discrepancy, negotiate.

Document diminished value. Get an appraisal showing your car’s diminished value after the accident. This is a real loss you may be entitled to recover.

Be careful what you say to the adjuster. Remember, if they’re handling both claims, everything you say about the accident and your condition is being noted for use in your injury claim.

When Low Property Damage Doesn’t Mean Low Injuries

If your property damage is low but your injuries are real, you need to be prepared to explain that disconnect. Here are arguments that work:

- The physics of the collision. Not all forces transfer to visible vehicle damage. Modern bumpers are designed to absorb impacts up to certain speeds with minimal visible damage—but that doesn’t mean no force was transferred to occupants.

- Your position at impact. Were you turned, reaching for something, looking in a mirror? Atypical positions make you more vulnerable to injury even in low-speed collisions.

- The nature of your specific injuries. Some injuries—particularly to the cervical spine, head, and joints—can occur at relatively low force levels, especially in people with certain risk factors.

- Medical evidence. If you have objective medical findings—imaging abnormalities, documented physical findings, treatment records showing consistent complaints and improvement—that evidence speaks louder than a repair estimate.

- Expert testimony. In litigation, biomechanical experts and accident reconstructionists can explain why low vehicle damage doesn’t preclude real injuries. This testimony can be powerful in countering the insurance company’s assumptions.

The Bottom Line

Don’t let the insurance company’s eagerness to settle your property damage claim quickly trap you into a weaker position on your injury claim.

That fast check for your car repairs comes with strings attached—strings that may bind you to a low number that undermines your ability to recover fair compensation for your injuries.

Take your time. Document everything. Understand what you’re agreeing to. And recognize that the insurance company’s interests and your interests are not aligned, even when they’re handling something as seemingly straightforward as getting your car fixed.

About the Author

Chi Nguyen is a Houston personal injury attorney dedicated to helping accident victims understand their rights and receive fair compensation under Texas law. With extensive experience representing injured Texans, Attorney Nguyen combines legal expertise with a commitment to client education and empowerment.