Table of contents

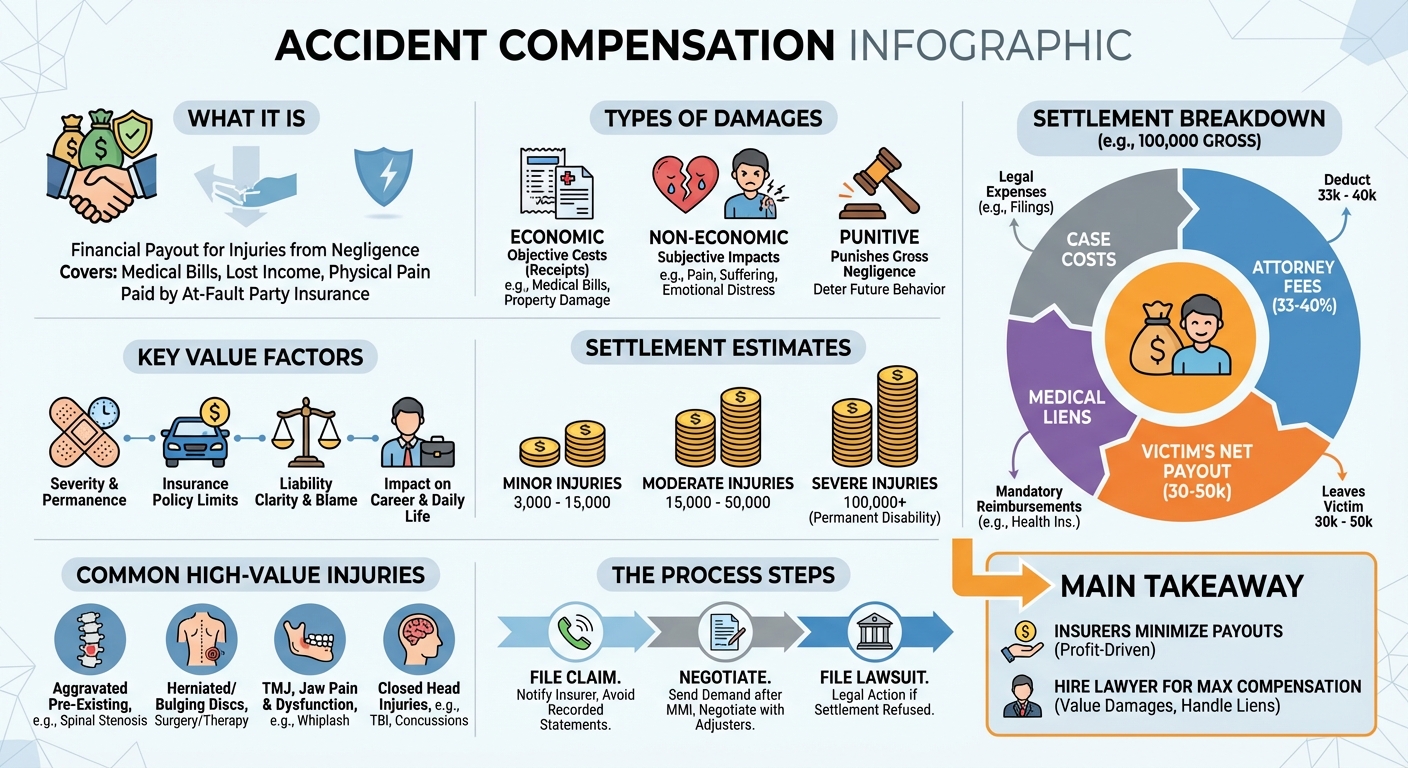

Accident compensation is the financial payout awarded to victims injured by someone else’s negligence. It typically covers two main categories: economic damages for calculable losses like medical bills and lost wages, and non-economic damages for subjective losses such as pain, suffering, and emotional distress.

The Complete Guide to Accident Compensation: Types, Payouts, and Process

If you have been injured due to someone else’s negligence, navigating the aftermath can be overwhelming. Between mounting medical bills, lost income, and physical pain, securing fair financial recovery is critical. This guide breaks down everything you need to know about accident compensation, from the types of damages available to how your final settlement is calculated.

What is accident compensation?

Accident compensation is the financial recovery awarded to a victim who suffers injuries or property damage due to another party’s negligence. This compensation, typically paid by the at-fault party’s insurance company, is designed to cover medical bills, lost wages, and pain and suffering resulting from the incident.

Types of Compensation You Can Claim After an Accident

In personal injury law, compensation is divided into specific categories based on the type of loss you have experienced. Understanding these categories is the first step in valuing your claim.

Economic Damages (Special Damages)

Economic damages reimburse you for the objective, out-of-pocket financial losses caused by the accident. Because these come with receipts and invoices, they are highly calculable. Common economic damages include:

- Medical Expenses: Emergency room visits, surgeries, physical therapy, and future medical care.

- Lost Wages: Income lost while recovering, as well as loss of future earning capacity if you are permanently disabled.

- Property Damage: The cost to repair or replace your vehicle and other personal property.

Non-Economic Damages (General Damages)

Non-economic damages compensate you for the subjective, intangible impacts of the accident. Though harder to calculate, they often make up the largest portion of a severe injury settlement. These include:

- Pain and Suffering: Physical discomfort and agony caused by your injuries.

- Emotional Distress: Anxiety, depression, PTSD, and loss of sleep.

- Loss of Consortium: The negative impact the injury has on your relationship with your spouse.

Punitive Damages (Exemplary Damages)

Unlike economic and non-economic damages, punitive damages are not meant to compensate the victim. Instead, they are designed to punish the at-fault party for gross negligence or intentional misconduct (such as drunk driving) and deter similar behavior in the future.

How much compensation can you get for a car accident?

The compensation you can get for a car accident varies widely based on injury severity. Minor accidents may settle between $3,000 and $15,000, while moderate injuries often yield $15,000 to $50,000. Severe accidents involving permanent disability or catastrophic injuries can result in settlements exceeding hundreds of thousands of dollars.

Key Factors That Influence Your Settlement Value

No two accidents are exactly alike. Insurance adjusters and attorneys evaluate several factors to determine a claim’s worth:

- Severity and Permanency of Injuries: Long-term or permanent injuries command higher payouts.

- Insurance Policy Limits: You generally cannot recover more than the at-fault driver’s policy limits unless other liable parties are identified.

- Clarity of Liability: If you share partial blame for the accident, your compensation may be reduced under comparative negligence laws.

- Impact on Daily Life: How the injury affects your career, hobbies, and independence.

How much of a $100K settlement will I get?

From a $100,000 settlement, you will typically take home between $30,000 and $50,000. After deducting standard attorney contingency fees (usually 33% to 40%), case expenses, and outstanding medical liens or health insurance subrogation claims, the remaining balance is disbursed directly to you.

Breaking Down Attorney Fees, Medical Liens, and Case Costs

Understanding the deductions from a gross settlement helps manage expectations:

- Attorney Fees: Most personal injury lawyers work on a contingency fee basis, taking one-third (33.3%) of the settlement if resolved before litigation, or up to 40% if a lawsuit is filed.

- Case Costs: These are out-of-pocket expenses advanced by your lawyer, such as court filing fees, expert witness fees, and medical record retrieval costs.

- Medical Liens: Your health insurance, Medicare, or medical providers who treated you on a letter of protection (LOP) must be reimbursed from the settlement funds.

Calculating Your Net Take-Home Compensation

Here is a simplified example of how a $100,000 settlement might be distributed:

| Category | Estimated Amount |

|---|---|

| Gross Settlement | $100,000 |

| Attorney Fees (33.3%) | -$33,333 |

| Case Expenses | -$2,500 |

| Medical Liens/Bills | -$25,000 |

| Net to Client | $39,167 |

Common Injuries and Their Impact on Compensation

The specific nature of your injury plays a massive role in the compensation process. Insurance companies scrutinize medical records to verify that the accident directly caused your condition.

Can a car accident cause spinal stenosis?

Yes, a car accident can cause or aggravate spinal stenosis. While spinal stenosis is often a pre-existing degenerative condition, the severe trauma of a car crash can accelerate the narrowing of the spinal canal or cause immediate symptomatic flare-ups, making you eligible for compensation for the worsened condition.

Other High-Value Injuries (Herniated Discs, TMJ, Closed Head Injuries)

Insurance companies often try to downplay certain injuries, but with proper medical documentation, they can result in substantial compensation:

- Herniated and Bulging Discs: Often requiring physical therapy, epidural injections, or surgical intervention.

- TMJ Injuries: Jaw pain and dysfunction frequently overlooked as a consequence of whiplash.

- Closed Head Injuries: Traumatic brain injuries (TBIs) and concussions that may not show up on initial scans but cause long-term cognitive issues.

How the Accident Compensation Process Works

Securing fair compensation is rarely as simple as submitting a bill to the insurance company. It involves a strategic, multi-step process.

Filing the Initial Insurance Claim

The process begins by notifying the at-fault party’s insurance company that you are pursuing a claim. During this phase, you should avoid giving recorded statements, as adjusters often use these to find inconsistencies and minimize your payout.

Negotiating with Insurance Adjusters

Once you reach Maximum Medical Improvement (MMI), your attorney will send a comprehensive demand letter outlining your injuries, damages, and a requested settlement amount. This triggers a series of negotiations. Adjusters will typically respond with a lowball initial offer to test your willingness to settle quickly.

When Settlement Fails: Filing a Lawsuit

If the insurance company refuses to offer a fair settlement, your attorney may recommend filing a personal injury lawsuit. Entering the litigation phase opens the door to formal discovery, depositions, and mediation. Often, simply filing a lawsuit puts enough pressure on the insurance company to offer a fair settlement before the case ever reaches a jury.

Why You Need a Personal Injury Lawyer to Maximize Your Compensation

Insurance companies are for-profit businesses; their primary goal is to minimize your accident compensation. A skilled personal injury lawyer levels the playing field. They know how to properly calculate your economic and non-economic damages, negotiate aggressively with adjusters, and navigate complex medical liens to ensure you walk away with the maximum possible net settlement.