Table of contents

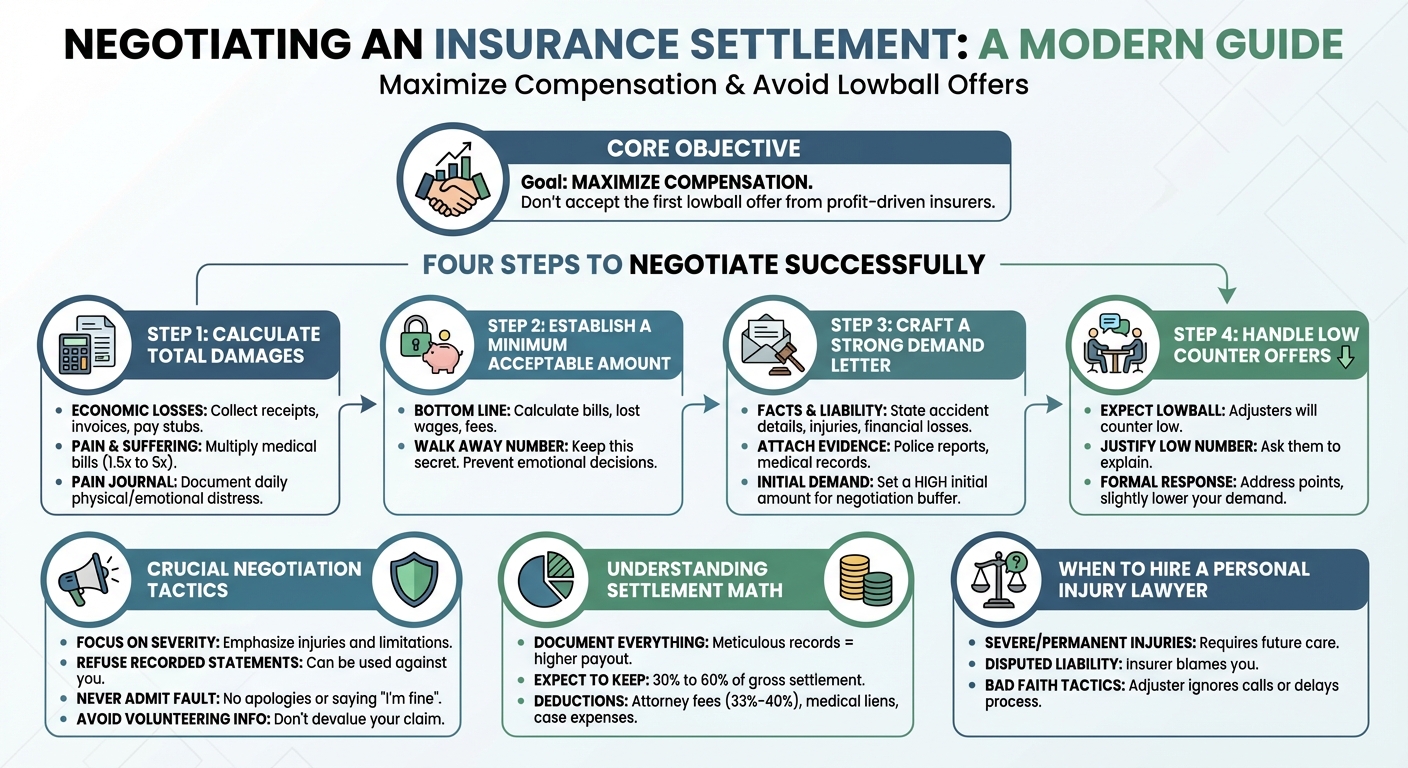

To negotiate an insurance settlement effectively, start by calculating your total damages and setting a minimum acceptable payout. Send a detailed demand letter with a high initial anchor. When the adjuster responds with a lowball offer, ask them to justify their number, then reply with a firm, evidence-based counter-offer.

How to Negotiate an Insurance Settlement: The Ultimate Step-by-Step Guide

Insurance companies are for-profit businesses. Their primary goal is to resolve claims quickly and for as little money as possible. If you have been injured in an accident, accepting the first offer from an insurance adjuster is rarely in your best interest. Negotiating a fair insurance settlement requires preparation, patience, and a clear understanding of the value of your claim. This guide breaks down the exact steps you need to take to level the playing field and secure the compensation you deserve.

Step 1: Calculate Your Total Damages and Gather Evidence

Before you can negotiate, you must know exactly how much your claim is worth. This requires compiling a comprehensive list of all your damages, backed by hard evidence.

Documenting Medical Bills and Lost Wages

Economic damages are your quantifiable financial losses. To prove these, you must gather every receipt, invoice, and pay stub related to your accident. This includes emergency room visits, physical therapy, prescription medications, medical equipment, and any future medical care you may require. Additionally, secure a letter from your employer detailing the exact number of hours and wages you lost while recovering.

Calculating Pain and Suffering

Non-economic damages compensate you for physical pain, emotional distress, and loss of enjoyment of life. Because these are subjective, insurance companies often use a multiplier method to calculate them. They will multiply your total medical bills by a number (typically between 1.5 and 5) based on the severity of your injuries. Keeping a daily pain journal detailing how the injury impacts your daily routine is crucial evidence for this calculation.

Step 2: Establish Your Minimum Acceptable Settlement Amount

Before you send a demand letter or speak to an adjuster, determine your bottom line. This is the absolute minimum amount you are willing to accept to settle the claim. Factor in your medical bills, lost wages, pain and suffering, and any attorney fees or medical liens. Keep this number strictly to yourself. Having a firm walk-away number prevents you from making emotional decisions or caving to pressure when the adjuster makes a lowball offer.

Step 3: Craft and Send a Strong Demand Letter

The demand letter officially initiates the negotiation process. It outlines your case, details your injuries, and states the amount of money you are requesting to settle the claim.

What to Include in Your Demand Letter

Your letter should be professional, concise, and factual. It must include a clear summary of the accident, an explanation of why the insured party is legally at fault, a detailed list of your injuries and medical treatments, an itemized list of your financial losses, and a specific monetary demand. Attach copies of all supporting documents, such as police reports and medical records.

Setting the Initial Anchor High

Your initial demand should be significantly higher than your minimum acceptable settlement amount. This creates a negotiation buffer. By setting a high initial anchor, you give yourself room to make concessions while still landing on or above your target number. However, the demand must remain realistic and justifiable based on your documented evidence.

Step 4: How to Respond to a Low Settlement Offer

Insurance adjusters almost always respond to a demand letter with a low counter-offer. This is a standard negotiation tactic designed to test your resolve and see if you are desperate for quick cash.

Ask the Adjuster to Justify Their Number

Do not immediately drop your demand. Instead, ask the adjuster to explain exactly how they arrived at their figure. Request specific reasons for why they are undervaluing your claim. Take detailed notes during this conversation. If they point out a weakness in your claim, such as a missing medical record, you now know exactly what additional evidence you need to provide.

Drafting Your Counter-Offer Letter

Once you understand their reasoning, write a formal counter-offer letter. Address their specific points, reiterate the strength of your evidence, and lower your initial demand slightly. This signals that you are willing to negotiate but are confident in the value of your claim. This back-and-forth process may take several rounds before you reach an agreeable figure.

Crucial Tactics for Dealing with Insurance Adjusters

Adjusters are trained negotiators who handle hundreds of claims a year. To protect your claim, you must understand their tactics and control the flow of information.

What should I not say during settlement?

During settlement negotiations, never admit fault, apologize, or say you are “fine” or “feeling better.” Do not agree to give a recorded statement without legal counsel, and never disclose your minimum acceptable settlement amount. Volunteering unnecessary information gives the insurance adjuster leverage to devalue your claim.

Emphasize the Severity of Your Injuries

Throughout the negotiation, continually steer the conversation back to the physical and emotional toll the accident has taken on your life. Remind the adjuster of the specific painful treatments you endured and the permanent limitations you now face. Humanizing your claim makes it harder for them to treat you as just another file number.

Refusing to Provide a Recorded Statement

Insurance adjusters will often pressure you to provide a recorded statement shortly after the accident. You are generally under no legal obligation to do so for the at-fault party’s insurance. These statements are often used to trap you into contradicting yourself or downplaying your injuries. Politely decline and state that your demand letter and medical records speak for themselves.

Understanding Settlement Math and Payouts

Understanding how settlement funds are distributed is essential for setting realistic expectations.

How to get the most out of an insurance settlement?

To get the most out of an insurance settlement, meticulously document all economic and non-economic damages, refuse the first lowball offer, and set a high initial anchor in your demand letter. Maintaining patience and hiring an experienced personal injury attorney can also significantly maximize your final payout.

How much of a $100K settlement will I get?

If you receive a $100,000 settlement, you will typically take home between $30,000 and $60,000. This net amount depends on standard deductions, including your personal injury attorney’s contingency fee (usually 33% to 40%), outstanding medical liens, and case expenses like expert witness fees or court filing costs.

What are the top 3 claim settlement ratios?

The top three claim settlement ratios generally refer to an insurer’s claim settlement rate, claim denial rate, and claim processing time. High settlement ratios indicate an insurance company pays out a large percentage of filed claims, which is a strong indicator of their reliability and willingness to negotiate fairly.

When to Negotiate Yourself vs. When to Hire a Personal Injury Lawyer

While minor claims with clear liability and minimal medical bills can often be handled without a lawyer, complex cases require professional legal representation.

Signs You Need an Attorney to Take Over

- Severe or Permanent Injuries: If your injuries require ongoing care or impact your ability to work, calculating future damages is complex and requires expert testimony.

- Disputed Liability: If the insurance company claims you were partially or fully at fault, an attorney can help prove liability and protect your rights.

- Bad Faith Tactics: If the adjuster is ignoring your calls, delaying the process unreasonably, or refusing to make a fair offer despite overwhelming evidence, it is time to hire a lawyer to litigate the case.