Table of contents

I’ve spent years sitting across the table from insurance adjusters, and I’ve learned something that changed how I approach every case:

The person on the other side of that phone call isn’t working for you. They’re working against you.

That’s not cynicism. It’s just business.

When I started practicing personal injury law in Houston, I assumed insurance companies operated like most businesses—trying to do right by their customers while also making a profit. What I discovered through years of negotiations, depositions, and trials is a system designed from the ground up to pay you as little as possible, as slowly as possible.

Today, I want to share what I’ve learned—not to scare you, but to prepare you. Because once you understand how this game is actually played, you can protect yourself.

The Business Model You Need to Understand

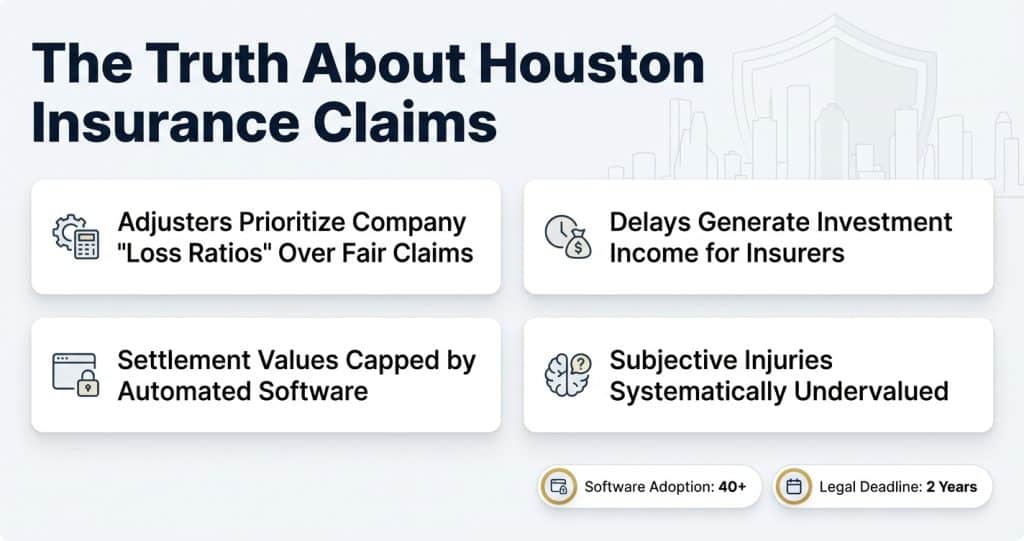

Insurance companies make money in ways most people don’t think about.

Yes, they collect premiums. But more importantly, they invest those premiums before paying out claims. The industry calls this “the float”—the time between when they collect your money and when they have to pay it back out.

-

Every day your settlement sits unpaid is another day they’re earning returns on funds that should be in your pocket.

-

Every month your claim drags on represents additional investment income for the company.

This isn’t a conspiracy theory—it’s their publicly acknowledged business model.

When you understand this, the delays start making sense:

-

Unreturned phone calls

-

Repeated requests for documents you’ve already provided

-

Endless “reviews” and “evaluations”

These aren’t just inefficiencies. They’re profitable.

I’ve watched adjusters let claims sit for months, making just enough contact to keep the file technically active. I’ve seen the same medical records requested multiple times, supposedly because earlier copies were “incomplete” or “illegible.”

Each delay costs you money and earns them interest.

Why Your Adjuster Seems Friendly—but Isn’t Helping

The adjuster assigned to your claim may genuinely be a nice person. Many of them are.

But their job isn’t to help you—it’s to minimize what their company pays.

Think about their incentives:

-

Adjusters aren’t rewarded for paying claims quickly

-

They’re evaluated on loss ratios—how much they pay out versus how much comes in

-

An adjuster who consistently pays full value doesn’t last long in the industry

Through litigation, I’ve reviewed internal insurance documents that spell this out clearly.

Adjusters are trained to:

-

Look for ways to reduce claim value

-

Use conversation scripts to push claimants toward low settlements

-

Identify who will fight—and who will fold

Some files even include notes like:

-

“Claimant appears desperate for money”

-

“Frustrated with attorneys”

-

“Unsophisticated about the claims process”

The more vulnerable you seem, the lower the offer.

The Computer Program Deciding Your Fate

Most people are shocked when they learn this:

Your claim value is largely decided by software.

Major insurance companies use computer programs to evaluate injury claims. The most well-known is Colossus, used by more than 40 insurers.

Adjusters enter:

-

Injury type

-

Treatment length

-

Medical costs

-

Location

The software then generates a settlement range.

That range becomes the ceiling for what you’ll be offered.

The problem?

-

Software doesn’t know your career ended

-

It doesn’t understand daily pain

-

It doesn’t care about lost hobbies, relationships, or quality of life

It sees codes and averages, not people.

Even worse, adjusters often can’t deviate much from what the system recommends. Their performance reviews, raises, and promotions depend on it.

So when you negotiate, you’re often not negotiating with a person—you’re negotiating with an algorithm.

Injuries the System Systematically Undervalues

Over the years, I’ve seen clear patterns in which injuries are consistently undervalued:

Neck & Back Injuries

-

Especially when MRIs don’t show “dramatic” findings

-

Bulging discs are often dismissed

-

Pain and functional loss are ignored if imaging isn’t extreme

Closed Head Injuries

Symptoms like:

-

Headaches

-

Memory loss

-

Concentration problems

-

Mood changes

-

Sleep disturbances

These are classic TBI signs—but because they’re “subjective,” the system discounts them.

Soft Tissue Injuries in Low-Speed Collisions

Insurance companies push the myth that:

“Minor crash = minor injury”

That’s simply not true.

Human bodies don’t move like cars. Position, rotation, and timing matter—but algorithms don’t understand physics or biomechanics.

Common Tactics Used Against You

Here are tactics I see repeatedly:

1. The Lowball Anchor

The first offer is intentionally insulting.

Why? Because the first number sets the psychological tone for negotiations.

2. The Nickel-and-Dime Delay

They request documents one at a time instead of all at once:

-

Medical records

-

Bills

-

Employer verification

-

Old records

Each request delays your claim.

3. The Vanishing Adjuster

Just as progress starts, your adjuster is “reassigned.”

The new one needs time to “get up to speed.”

This can happen multiple times.

4. The Carrot and Stick

They pay:

-

Property damage quickly

-

Medical payments coverage

But delay the injury claim—the part worth real money.

5. The Experience Gap

You handle one major claim in your life.

They handle thousands.

They know:

-

How long most people wait

-

When frustration peaks

-

When low offers get accepted

What Actually Helps Your Case

Focus on Getting Better

Follow medical advice.

Attend therapy.

Take prescribed medication.

Claimants who genuinely try to recover are taken more seriously—by insurers and juries.

Document Everything

Keep:

-

A symptom journal

-

Medical paperwork

-

Bills

-

Emails and letters

-

Notes from phone calls

Organization matters.

Be Careful With Early Settlements

Quick checks can lock in low expectations.

Low vehicle damage = “minor injury” arguments later.

Watch What You Say

Every conversation is an investigation.

Be honest—but careful.

-

Don’t speculate

-

Don’t minimize pain

-

Don’t give recorded statements lightly

Know Your Deadlines

In Texas, you generally have two years to file a lawsuit.

That time goes faster than you think.

When You Should Get Help

Not every accident requires an attorney.

But you should at least consult one if:

-

Injuries are serious or ongoing

-

Liability is disputed

-

You’re pressured to settle early

-

The adjuster is stalling or unresponsive

-

Offers don’t reflect real losses

-

You have pre-existing conditions

-

A commercial vehicle is involved

-

Multiple parties are involved

Most consultations are free.

The Bottom Line

Insurance companies aren’t evil.

They’re businesses protecting their bottom line.

But their interests and yours are fundamentally opposed.

They want to pay as little as possible.

You deserve fair compensation for injuries that weren’t your fault.

Understanding how the system works—delays, software, tactics—puts you in control.

Knowledge is power.

About the Author

Chi Nguyen is a Houston personal injury attorney dedicated to helping accident victims understand their rights and receive fair compensation under Texas law. With extensive experience representing injured Texans, Attorney Nguyen combines legal expertise with a commitment to client education and empowerment.